"Exide: Running on low power")

The Exide Industries' stock has been touching 52-week lows in the past week and has lost 19 per cent in a month and a half. The fall is on a poor September quarter performance and earnings downgrades thereafter. Analysts say the company, which saw its volumes fall in the quarter, is losing to Amara Raja.

Given the poor volume growth in the automobile original equipment manufacturer (OEM) space and the muted show in the industrial segment, research houses have cut FY14 earnings estimate 15 per cent. While most have a buy on Raja and Exide, the former is preferred. Exide is trading at 14.6 times its FY15 estimates. Given target upwards of Rs 125 and the steep correction in the stock (Rs 114), there is limited upside in a year. The trigger will be volume gains and margin improvement.

Analysts say unless the company cuts the premium it charges on batteries (10 per cent compared to Amara Raja), it could lose more market share. Joseph George and Kevin Mehta of IIFL Institutional Equities say given the inefficiencies in its cost structure and Raja's increasing brand recall, Exide may have to settle for lower pricing premium and, hence, lower earnings before interest, taxes, depreciation and amortisation (Ebitda) margin than Raja’s. The company has been focusing on margins and has taken a series of price rises in a year.

However, after four rises, five to seven per cent each since the start of November 2012, the company dropped prices two to five per cent at the start of November 2013. Both have been raising prices on higher lead prices and falling rupee. The likely causes for the recent price cut by Exide could be the rupee recovery, lower lead prices year-on-year or market-share loss.

In a recent concall, the management said the market share in the auto segment was intact and it would like to retain its share without compromising on margins. IIFL analysts, however, said the market-share loss forced the company to cut prices. While the firm did not comment on its future pricing strategy, what would come to its aid is the stable rupee and the 3.5 per cent to four per cent fall in lead prices year-on-year (sequentially flat).

Double-digit growth in the replacement segment and pricing power were the key positives for Exide. However, growth worries in some of its cyclical businesses (auto OEM, industrial) could negate this. Kaushal Maroo of Emkay Global says while the positives have been in play in three quarters, higher-than-anticipated weakness in the cyclical portions of the business has offset these.

While the company did not indicate the volume growth numbers for the quarter, the sharp fall in lead consumption (25 per cent sequential decline in tonnage terms) indicates volumes have taken a knock. IIFL estimates while Exide recorded a volume growth of six to eight per cent in the auto replacement market, Raja recorded a jump of 18-23 per cent.

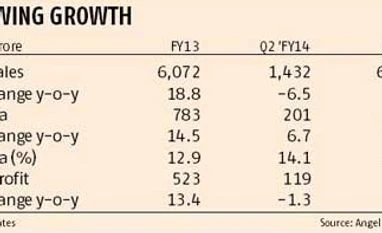

The poor volume performance of the inverters, UPS and OEM auto segments led to the significant underperformance at the operating profit level. While revenues were down six per cent year-on-year to Rs 1,432 crore, operating profit at Rs 200 crore was up six per cent year-on-year (but 14-19 per cent lower than analysts' estimates).

On a sequential basis, both revenues and operating profits were down 12-23 per cent. Ebitda margins, up 180 basis points year-on-year to 14.1 per cent, fell sequentially. With the exception of the June quarter (16.1 per cent), the Ebitda margins have been in the range of 11.2 per cent to 14.9 per cent in seven quarters. Analysts estimate the company will achieve between 14.5 and 5 per cent Ebitda margins for FY14. While the company achieved a margin of 15.2 per cent in the first half of the financial year, it has a target of a 16 per cent margin.

Given the poor volume growth in the automobile original equipment manufacturer (OEM) space and the muted show in the industrial segment, research houses have cut FY14 earnings estimate 15 per cent. While most have a buy on Raja and Exide, the former is preferred. Exide is trading at 14.6 times its FY15 estimates. Given target upwards of Rs 125 and the steep correction in the stock (Rs 114), there is limited upside in a year. The trigger will be volume gains and margin improvement.

Analysts say unless the company cuts the premium it charges on batteries (10 per cent compared to Amara Raja), it could lose more market share. Joseph George and Kevin Mehta of IIFL Institutional Equities say given the inefficiencies in its cost structure and Raja's increasing brand recall, Exide may have to settle for lower pricing premium and, hence, lower earnings before interest, taxes, depreciation and amortisation (Ebitda) margin than Raja’s. The company has been focusing on margins and has taken a series of price rises in a year.

However, after four rises, five to seven per cent each since the start of November 2012, the company dropped prices two to five per cent at the start of November 2013. Both have been raising prices on higher lead prices and falling rupee. The likely causes for the recent price cut by Exide could be the rupee recovery, lower lead prices year-on-year or market-share loss.

In a recent concall, the management said the market share in the auto segment was intact and it would like to retain its share without compromising on margins. IIFL analysts, however, said the market-share loss forced the company to cut prices. While the firm did not comment on its future pricing strategy, what would come to its aid is the stable rupee and the 3.5 per cent to four per cent fall in lead prices year-on-year (sequentially flat).

Double-digit growth in the replacement segment and pricing power were the key positives for Exide. However, growth worries in some of its cyclical businesses (auto OEM, industrial) could negate this. Kaushal Maroo of Emkay Global says while the positives have been in play in three quarters, higher-than-anticipated weakness in the cyclical portions of the business has offset these.

While the company did not indicate the volume growth numbers for the quarter, the sharp fall in lead consumption (25 per cent sequential decline in tonnage terms) indicates volumes have taken a knock. IIFL estimates while Exide recorded a volume growth of six to eight per cent in the auto replacement market, Raja recorded a jump of 18-23 per cent.

The poor volume performance of the inverters, UPS and OEM auto segments led to the significant underperformance at the operating profit level. While revenues were down six per cent year-on-year to Rs 1,432 crore, operating profit at Rs 200 crore was up six per cent year-on-year (but 14-19 per cent lower than analysts' estimates).

On a sequential basis, both revenues and operating profits were down 12-23 per cent. Ebitda margins, up 180 basis points year-on-year to 14.1 per cent, fell sequentially. With the exception of the June quarter (16.1 per cent), the Ebitda margins have been in the range of 11.2 per cent to 14.9 per cent in seven quarters. Analysts estimate the company will achieve between 14.5 and 5 per cent Ebitda margins for FY14. While the company achieved a margin of 15.2 per cent in the first half of the financial year, it has a target of a 16 per cent margin.