"FY18 starts with big earnings cut")

Earnings’ downgrades have become a regular feature in Indian stock markets. However, the infection that caught India Inc about three years earlier is now manifesting into a disease.

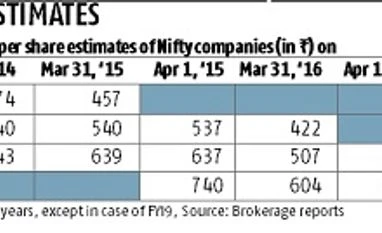

If FY14-17 estimates were marked by a 10-27 per cent earnings’ downgrade, 2017-18 (starting April 1) begins with a 40 per cent downgrade in earnings estimates for Nifty companies. This is the highest in the past four years. The consensus in a Bloomberg poll, pegs Nifty companies’ earnings per share (EPS) at Rs 526.4 in FY18.

Two years earlier, the EPS forecast was Rs 739.7. When prospects began to look weak in March 2016, the Street slashed its target EPS by 20.5 per cent for FY17 and 18.4 per cent for FY18. The next big round of earnings alteration happened after demonetisation, which impelled the Street to reduce its EPS target by 11 per cent for FY17 and 11.5 per cent for FY18.

And, experts such as Saurabh Mukerjea and Sanjay Mookim warn of more earnings downgrade.

In an interaction last month, Mukerjea, chief executive at Ambit Capital, said FY18 might be no different from the previous cycles, where the Street starts the year with high hope and tempers this in the course of the year.

Sanjay Mookim, India equity strategist at Bank of America Merrill Lynch, says his brokerage expects FY18 earnings to grow by 12-13 per cent for Nifty companies. The consensus is still for 20 per cent growth; analysts polled on Bloomberg peg the FY18 Nifty EPS at Rs 526.4 versus the FY17 one of Rs 436.4. Therefore, Mookim believes there could be a meaningful downgrade, given that the Street is looking at higher growth.

Amar Ambani, head of research at IIFL, who concurs with the view, explains that analysts tend to paint a rosy picture of the sectors they track. “Even for a beaten-down sector like telecom, analysts have remained positive on earnings growth.”

Still, FY18 might see earnings grow, with a recovery in profits of banks and commodity-linked companies in the metals and oil & gas space. However, expectations of 20 per cent growth seem over-stated, as in the past.

Ambani adds that information technology stocks, too, might surprise the Street positively if they manage to deliver 10 per cent growth in FY18. “The consensus for now is building just about seven per cent growth for the sector,” he says.

E: Estimates; NA: not applicable/available, * over two years, except in case of FY19, Source: Brokerage reports Compiled by BS Research Bureau

However, the list of stocks which can throw negative surprises is longer. Experts are cautious on those of consumer discretionary and fast moving consumer goods entities. “The market is misinterpreting growth. When companies talk of normalisation, they refer to a restoration to previous levels. Equities need a restoration of growth,” Mookim warns.

The likely implementation of a national goods and services tax from July 1 might further add to earnings pressure, as it could cause a shift in consumer behaviour. “We don’t know yet how the shift will be,” he says.

As for consumer discretionary, experts are wary of when a strong demand revival can happen. For now, their channel checks indicate six months deferment in purchases. Experts also flag pressure on operating profit margins in FY18. Mookim explains, “In our analysis of 500 companies, almost every industry and sector is at a high base on operating margins. There is no way these can be sustained.” When operating profit margins start faltering, it could also trigger earnings downgrade. “Sell-side analysts aren't factoring for lower margins,” he warns.

However, despite these pressures, Pankay Pandey, head of research at ICICI Securities, feels stock prices might fall by much, even if earnings disappoint. “Equities will do well, irrespective of what earnings or valuations are, simply because the competing asset classes don’t find much favour. Money will continue to chase stocks,” he says.

This view is in sync with the current market mood. Whether rationality would set into equities is a bigger question. Headwinds in the form of further rate hikes by the US Federal Reserve, a subdued demand environment and a delicate bad loan issue at home are being underestimated, say experts.

What the Street is perhaps ignoring is that even as earnings have been consistently downgraded in the past few years, the actual earnings have come even below such estimates.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in