"Higher margin norms likely to affect derivatives segment volumes")

In what may impact volumes and reduce leverage in the market, brokers will collect much higher margins from clients trading in the derivatives segment from Monday.

Over the past few months, the Securities and Exchange Board of India (Sebi) has raised the margin requirement thrice, effectively increasing it by 40-50 per cent.

Options writers, especially those writing out of the money options, and arbitrageurs, who attempt to profit from price inefficiencies, will be hit the most.

"Such a large margin increase has come as a shock because of the quantum of the hike, at such a short notice. Recently, exchanges levied Additional Surveillance Margin (ASM), which was less than half the current proposed increase and was spread out over a three-month period. We hope the regulatory authorities will provide more time to adjust to the increased margins, and thus avoid unnecessary volatility in the markets due to unwinding," said a large options trader who deals with multiple brokers.

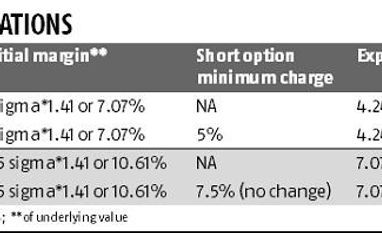

From June 1, 2018, clearing or trading members were mandated to include initial margin, exposure margin or extreme loss margin, mark-to-market settlements and calendar spread margin. On September 1, ASM was introduced in addition to SPAN (standard portfolio analysis of risk) and exposure margins.

SPAN margins are charged to cover for the worst possible movement in the contract for a single day. The new requirements, effective January 21, mandate a cover for volatility over two days. Exposure margins are charged over and above the SPAN margins, and will be increased to 4.24 per cent for index futures and options (F&O), and 7.07 per cent or 1.5 sigma (whichever is higher), for stock F&O.

Therefore, one lot of Nifty futures that earlier required around Rs 50,000 of SPAN in May to hold the position overnight, will now require Rs 1 lakh in the form of SPAN and exposure margins.

“The problem is the increase (in margins) has been quite steep and in quick succession,” said Zerodha CEO Nithin Kamath. “We need to find a way to give more margin benefit on hedged positions, which is currently missing, therefore encouraging people to move towards arbitrage and hedging from trading naked.”

Experts reckon there is no clarity on the steep increase in margins over the past few months. "Is it aimed at managing risk or curbing excessive speculation?" asked Deven Choksey, managing director of KR Choksey Investment Managers.

He added the derivatives market was currently dominated by those wanting to leverage or trade, and it was difficult for investors to effectively hedge risks: “There are artificially defined contract lots, the margins are on the higher side, and there is no delivery settlement to speak of.”

Sebi's December 17 circular states that the Principles for Financial Market Infrastructures has prescribed that the central counterparty (CCP) should adopt a margin system and parameters that are risk-based, and generate margin requirements sufficient to cover future risks.

It adds that a CCP should also consider the potential market liquidation costs that it assumes to incur while liquidating a participant’s portfolio.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in