"Hindalco, Vedanta top gainers as outlook improves for non-ferrous stocks")

Non-ferrous stocks, led by Hindalco and Vedanta, were among the key gainers on Monday on easing of trade war concerns after the G20 Summit. Hindalco and Vedanta closed up more than 3 per cent each as the US and China agreed to postpone new tariff levy for 90 days and hold further talks.

Aluminium, zinc, and lead prices on the London Metal Exchange have rebounded 1-4 per cent from their lows seen on last week. Kamal Kant Sahoo at Emkay Global feels decline in crude prices is also good news for metal players. He expects metal prices to improve and stabilise.

Aluminium remains the most preferred base metal looking at demand-supply constraints. The recent news flow on China production cuts too remains favourable. A recent Citi Research report highlighted that China’s Hongqiao Group, the world’s biggest aluminium producer, has been ordered to close up to 550,000 tonnes of annual smelting capacity this winter.

Earlier, sanctions on Russia’s Rusal and falling aluminium supply had kept analysts positive. Brokerages expect global demand for aluminium to rise 4 per cent (about 64 million tonne, or mt), while the production growth is pegged at 1 per cent (about 62.2 mt), which will leave a global deficit of 1.8 mt.

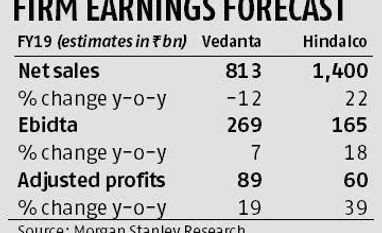

Positive alumunium price outlook bodes well for both Vedanta and Hindalco, the largest aluminium producers in the country. For Hindalco, its integrated operations in domestic market with Novelis (overseas subsidiary), which converts them to value-added products, bodes well, insulating it from input cost pressures.

Vedanta, however, has interests in zinc, lead, silver, and copper business and should benefit from these segments as well. Zinc contributes more than a fifth to revenues and remains the next key segment after aluminium, which contributes close to a third of the company’s overall revenues. Vedanta is expected to see increased production from Hindustan Zinc and international operations too driving its overall growth. Nevertheless, some concerns on zinc supplies exceeding demand is keeping analysts cautious.

Analysts at Morgan Stanley believe Hindalco's earnings find support as 65 per cent of operating profit is driven by the relatively stable downstream and copper segments, while upstream aluminum benefits from backward integration.

The positives for Vedanta, according to them, are a strong balance sheet. They are, however, cautious on the company as its projects are in a ramp-up phase and any production delays or higher costs could pose risks to earnings.

Further a benign zinc price outlook for 2019 and 2020 (segment accounts for 40 per cent of operating profit) is another concern. Thus, while Morgan Stanley remains cautious on Vedanta, its target price translates to an upside of about 16 per cent, from current levels of Rs203. For Hindalco, their target price of Rs295 means an upside of about 27 per cent from current price.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in