)

Inox Wind, India’s fourth-largest wind energy turbine generator (WTG) manufacturer, is coming out with a Rs 1,000-crore initial public offering (IPO) comprising a fresh issue of up to Rs 700 crore; the rest is an offer for sale by the promoter firm, Gujarat Flurochemicals. While retail investors will get a discount of Rs 15 a share on a price band of Rs 315-325, the offer looks fairly valued from a near-term perspective. But given the company’s strong record and long-term growth prospects, investors with a long-term horizon could subscribe.

Strong footing

Set up in FY10, Inox Wind is an integrated wind energy solutions provider. It manufactures and supplies equipment in this regard, sets up wind farms and makes these operational. It also provides turnkey solutions for wind power projects in India. While the company manufactures major components of WTGs, including nacelles, hubs, rotor blade sets and towers, at its in-house facilities, it has a technical collaboration with Austrian wind major AMSC, a Nasdaq-listed company, to manufacture a 2 Mw WTG in India. Inox has an exclusive and perpetual licence from AMSC, with current combined manufacturing capacity of 800 Mw at two manufacturing facilities — at Una in Himachal Pradesh and Ahmedabad in Gujarat. The company plans to double capacity by the end of FY16. Work at a plant in Madhya Pradesh is progressing well. Inox operates and maintains a large part of the projects it has commissioned, which lends significant confidence to its business.

Growing fast

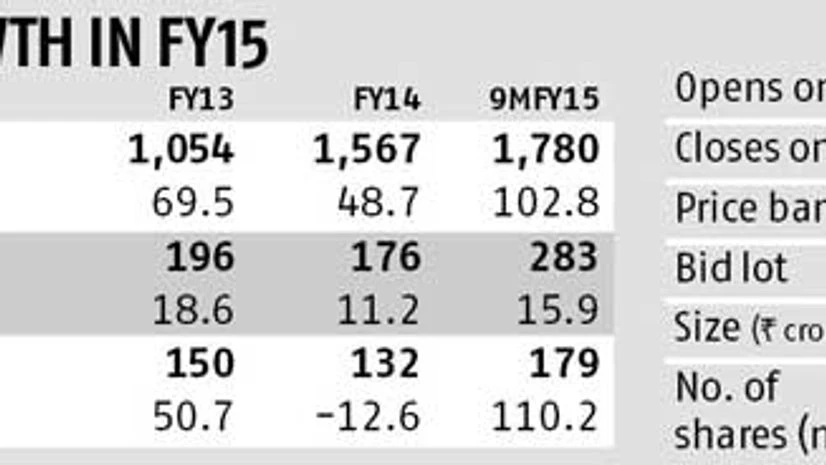

Since its inception, Inox Wind has delivered strong growth. In FY12, it sold 120 Mw (about 60 WTG) to group companies. Thereafter, third-party sales have continued to increase; these stood at 380 Mw in the nine months ended December 2014. From only Rs 7.8 crore in FY10, the company’s revenue increased to Rs 71.9 crore in FY11 and to Rs 1,567 crore in FY14. The company’s earnings before interest, tax, depreciation and amortisation has grown from a negligible level in FY10 to Rs 176 crore in FY14, while profit has grown at a compounded annual rate of 174 per cent during FY11-14.

Many triggers

Once again, the wind energy sector has received growth impetus from the government. This has reintroduced accelerated depreciation for windmills, besides raising generation-based incentives. Also, the new companies Act provides for spending on renewable energy and WTG to qualify as corporate social responsibility.

This is likely to boost demand and support Inox’s growth. The company plans to utilise the IPO proceeds for growing its business. Of the Rs 700 crore it plans to raise, Rs 150 crore is earmarked for manufacturing capacities, Rs 300 crore to cut its long-term working debt of Rs 750 crore, Rs 150 crore for investment in infrastructure and Rs 100 crore for general purposes.

As such, Inox’s strong growth is likely to continue, supported by a robust order book of 1;258 Mw. Its customer base includes companies such as Tata Power, Continuum Wind, Clean Wind Power (Hero Group) and ReNew Power.

Investment rationale

While the company’s record is good and its order book robust, a strong management adds to confidence. Other listed group companies such as Inox Leisure and Gujarat Fluorochemicals have also seen good growth.

Manish Bhatt, vice president and head (primary markets), Prabhudas Lilladher, says one should subscribe to the company’s issue. While a strong cash-rich promoter is positive, Inox’s leverage might also be phased off by FY16-17, says Bhatt. He adds considering the estimated growth for FY16-17, valuations are cheap.

For Inox, it will be important to keep working capital debt under control, as in the past, Suzlon Energy has seen debt issues affect its operations.

Analysts expect Inox’s return on equity to sustain at 27-30 per cent. Rahul Shah of Motilal Oswal Securities says one shouldn’t invest looking at the listing gains, but for the medium to long term. The brokerage firm expects Inox’s WTG sales to increase from 330 Mw in FY14 to about 600 Mw in FY15 and 1-1.2 Gw in FY16. The company’s operations and maintenance business also provides growth possibilities.