"Investors flock to direct plans, save crores")

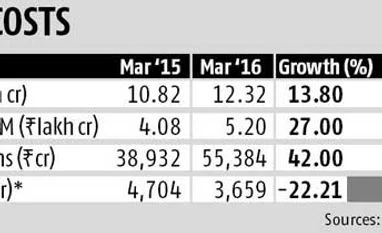

Sebi had in January 2013 asked mutual funds to offer such plans in all schemes. There would not be any distribution fees or trail fees paid to agents for such schemes. Because of this, expense ratios would be lower than regular plans. In the year ending March 2016, equity assets under management (AUM) in the direct channel went up 42 per cent to Rs 55,384 crore from Rs 38,932 crore. Across all schemes including debt, AUM from the direct channel went up from Rs 4.08 lakh crore to Rs 5.20 lakh crore, an increase of 27 per cent. In comparison, overall AUM of the industry grew at a much slower pace of 13.8 per cent to Rs 12.32 lakh crore from Rs 10.82 lakh crore. This has had an impact on the amount investors paid distributors as commission, say experts.

An analysis of Prime Database data on commission paid to 572 distributors by 40 AMCs showed there was a decrease in commission paid from Rs 4,704 crore in 2014-15 (FY15) to Rs 3,659 crore in FY16, a fall of 22.21 per cent.

Analysts feel this trend is likely to gather momentum in the coming years. Pranav Haldea, managing director, Prime Database, said, “A major reason for the fall in commission is the increasing popularity of the direct channel. This is likely to become stronger going forward.” N J India Invest was the largest distributor in FY16 having earned a commission of Rs 326 crore, followed by HDFC Bank (Rs 261 crore), ICICI Bank (Rs 170 crore), Kotak Mahindra Bank (Rs 166 crore) and Darshan Securities (Rs 160 crore).

Distributors said the movement towards direct channel is seen largely among larger investors such as corporations and HNIs. V Krishnan, president, Integrated Enterprises, said, “As far as mass retail is concerned, there is still no major shift towards the direct channel. These investors need handholding not only in choosing product but also in other aspects of managing the investment. It is the big transactions from corporates that has gone direct.” Distributors say other factors such as capping of upfront fee on closed ended funds at one per cent led to lower commissions in FY 16. Krishnan felt even if smaller investors take the direct route, “they will come back in a few months.”

Though distributors seek to play down the success of direct plans, an analysis of Prime Database data show there is a conflict of interest when MFs have in-house distributors as then such a distributor tends to and is incentivised to push schemes belonging to their group company, irrespective of whether these plans are good for investors. At the same time, certain MFs seem to rely heavily on their respective in-house distributors.