"IPO review: MEP Infra's risk-reward unfavourable")

MEP Infrastructure Developers (MEP) has come out with an Initial Public Offer (IPO) to raise Rs 324 crore, about 80 per cent of which will be utilised for repaying loans of its subsidiary, MIPL. The latter's debt was Rs 2,776 crore as on January 31.

The company is in the business of toll operations and operates road infrastructure projects. These include long-term OMT (operate-maintain-transfer) and BOT (build-operate-transfer) projects in Maharashtra, Gujarat, Rajasthan, Andhra, Tamil Nadu and West Bengal.

Among the notable large projects are the Mumbai Entry Points one, where it collects toll at five entry points into the city (toll plazas at Airoli, Vashi, Dahisar, Eastern Express Highway, Mulund and LBS Marg, Mulund). Such projects are long-term and have upfront payment to be made.

For instance, Mumbai Entry Points is a 16-year project, starting November 2010, for which MEP has given upfront payment of Rs 2,100 crore. While such projects are big enough and likely to have a positive bearing in the longer run, the high upfront payment has led to raising of substantial debt.

In this backdrop, high interest costs in the initial years and high amortisation has hit MEP’s profits. Analysts believe this particular project is so structured as to generate losses for the first few years, despite regular traffic growth. Another reason for losses widening in FY14 was the Chennai Bypass OMT.

The company suffered loss of revenue from this on account of certain force majeure issues arising from non-compliance with certain provisions of the project contract by National Highways Authority of India. It is likely to get compensation of up to Rs 150 crore.

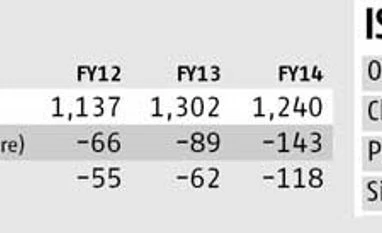

With stress on the balance sheet, the company’s finance costs have increased from Rs 5.3 crore in FY10 to Rs 143 crore in FY14, on a consolidated basis. Coupled with regular increase in depreciation and amortisation (Rs 126 crore in FY14 against Rs 46 lakh in FY10) and operating and maintenance expenses growing 2.5 times to Rs 801 crore in FY14, MEP reported loss before tax of Rs 143.2 crore in FY14 versus profit before tax at Rs 49 lakh in FY10.

Looking at the weak financials, despite reduction in debt after the IPO (and including the Chennai Bypass compensation), the wait for investors will be long. Although MEP has a large presence and a number of operational projects, break-even is crucial. The uncertainties regarding toll collection removal in Mumbai and consequent compensation to toll companies also exist. In view of these, investors could skip the offer.

The company is in the business of toll operations and operates road infrastructure projects. These include long-term OMT (operate-maintain-transfer) and BOT (build-operate-transfer) projects in Maharashtra, Gujarat, Rajasthan, Andhra, Tamil Nadu and West Bengal.

Among the notable large projects are the Mumbai Entry Points one, where it collects toll at five entry points into the city (toll plazas at Airoli, Vashi, Dahisar, Eastern Express Highway, Mulund and LBS Marg, Mulund). Such projects are long-term and have upfront payment to be made.

For instance, Mumbai Entry Points is a 16-year project, starting November 2010, for which MEP has given upfront payment of Rs 2,100 crore. While such projects are big enough and likely to have a positive bearing in the longer run, the high upfront payment has led to raising of substantial debt.

In this backdrop, high interest costs in the initial years and high amortisation has hit MEP’s profits. Analysts believe this particular project is so structured as to generate losses for the first few years, despite regular traffic growth. Another reason for losses widening in FY14 was the Chennai Bypass OMT.

The company suffered loss of revenue from this on account of certain force majeure issues arising from non-compliance with certain provisions of the project contract by National Highways Authority of India. It is likely to get compensation of up to Rs 150 crore.

With stress on the balance sheet, the company’s finance costs have increased from Rs 5.3 crore in FY10 to Rs 143 crore in FY14, on a consolidated basis. Coupled with regular increase in depreciation and amortisation (Rs 126 crore in FY14 against Rs 46 lakh in FY10) and operating and maintenance expenses growing 2.5 times to Rs 801 crore in FY14, MEP reported loss before tax of Rs 143.2 crore in FY14 versus profit before tax at Rs 49 lakh in FY10.

Looking at the weak financials, despite reduction in debt after the IPO (and including the Chennai Bypass compensation), the wait for investors will be long. Although MEP has a large presence and a number of operational projects, break-even is crucial. The uncertainties regarding toll collection removal in Mumbai and consequent compensation to toll companies also exist. In view of these, investors could skip the offer.