"LTCG tax and trade war: Markets head for worst 2-month drop since FY16")

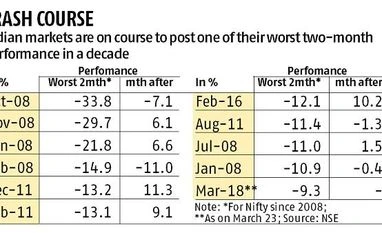

The benchmark Nifty is down 9.3 per cent since February, its fifth worst two-month decline since 2009. Broader markets too have seen sharp declines, with the BSE Midcap and Smallcap indices falling 14 per cent and 17 per cent, respectively, from their January peaks.

On a majority of occasions, domestic markets have witnessed a rebound following sharp two-month declines. This time, however, the chances of a sharp recovery in April look difficult as the market faces several global and domestic headwinds.

The trade-war between the US and China is prompting investors to flee from risky assets, such as equities, to safe-haven bets, such as gold and treasuries. On the domestic front, banking shares are reeling under the pressure of the Punjab National Bank fraud and tighter regulations. Financial stocks have the most weight in the benchmark indices.

Another risk for the markets is the spike in oil prices last week. Defying the slump in equities, Brent crude prices neared the $70 per barrel-levels, rising over 4 per cent during the week.

Political uncertainty is another factor that could keep market gains in check. Nomura, in a note last week, said the Indian markets haven’t fully priced in the political risk and the possibility of a reform stalemate. “Political uncertainty and noise are set to rise. Some consideration is needed to be assigned to the opposition parties performing better than 2014. We believe these political risks are currently underpriced,” it said, adding that “big-ticket reforms are less likely and a populist overtone is more likely".

The silver lining for the Indian markets has been the buying by foreign portfolio investors (FPIs). Despite, the market turmoil, FPIs have invested around Rs 120 billion in the domestic markets this month. However, most investments have come in primary market issuances and bulk deals in Tata Consultancy Services (TCS). This month, initial public offerings (IPOs) worth Rs 150 billion have hit the market.

Domestic brokerage Prabhudas Lilladher says Nifty could trade in a range between 9,640 and 10,500. On Friday, it closed at 9,998, the lowest since October 9. Despite the sharp correction, the Indian markets continue to trade above their long-term averages.

“We expect the market to remain soft in the near future. The MSCI India premium relative to MSCI Asia (ex Japan) is at 33 per cent against the 10-year average of 39 per cent,” says the brokerage.

Shane Oliver, head of the investment strategy, AMP Capital believes while volatility will continue to remain high, the broad trend could be positive as “a global recession is unlikely and earnings growth remains strong.”