4:21 PM

Radhika Rao, India Economist, DBS Bank on RBI policy

The guidance was cautious on the near-term inflation outlook, owing to higher oil prices, housing rent allowance increases, rising input prices, fiscal slippage risks and core pressures. However, this was counter-balanced by a negative output gap and the cuts in GST rates which are expected to partly ease price pressures. While the FY18 GVA estimate was maintained and growth has bottomed-out in 2Q, a downward revision remains on the cards.

Back on inflation, we expect the headline to settle within a broad 4-5% range, with base effects tempering the headline prints intermittently. While this closes the door for rate cuts, a clear bias towards rate hikes will require faster inflation to be accompanied by a strong turnaround in growth.

On this account, we see range-bound inflation whilst growth returns gradually, providing the central bank with the comfort to remain on-hold during this phase, not rushing to tighten policy. A modest fiscal slippage is expected but not a deviation from the consolidation path. Oil prices remain the most uncertain part of the price outlook

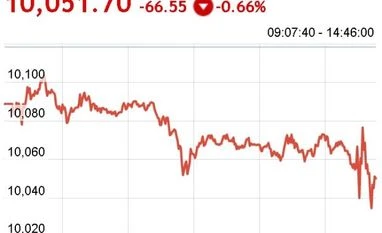

"Sensex ends 205 pts lower, Nifty below 10050 post RBI policy outcome")