"Matrimony.com IPO: Tie the knot but think long-term")

Low penetration levels, a sharp increase in smartphone and data usage and a well-established brand is expected to keep the growth momentum going for the country’s leading online matchmaking services company, Matrimony.com.

The biggest revenue trigger for the company is the size of the opportunity in a largely fragmented industry, both in the online and the offline space. The size of the market, according to KPMG, of unmarried individuals was 107 million in CY2016, of whom 63 million were actively looking for a partner. Of them, only 10 per cent (6 million) were active users of online matrimony. Given that the company has 3.08 million active users and a lot more people are opting to tap the online matrimony space, there is a large untapped market for the leader. With the base of mobile internet users expected to double from 2016 levels to just under 700 million by FY20, it should help the company. Besides Matrimony, the two other large players in the online space are Shaadi.com and Jeevansathi.com. Matrimony is ahead of the other two as it gets twice the unique visitors at 990,000, ten times more page views at 459 million and about five times more as far as the time spent on the site at 149 minutes.

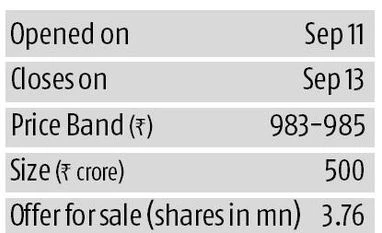

Given the brand strength, improving margins and opportunity for growth, most brokerages have given a subscribe recommendation for the IPO, which is asking for a valuation of 51 times its FY17 earnings. If FY18 numbers are annualised, the valuation multiple would be 35 times, while peers such as Info Edge (though strictly not comparable) are trading at 46 times on the same metric. The key risks include a lack of steady margin profile prior to FY17. Moreover a large 10 per cent discount to retail investors is also surprising given the retail portion is 10 per cent or Rs 50 crore. Investors can look at the issue but over a three-year period to benefit from the improving margin profile, which has shown a sharp increase only from FY17.

Revenue growth, according to the company, is a combination of increasing the number of profiles (currently 3.08 million), converting these to paid profiles and finally increasing the average transaction value. Profiles are expected to grow at 20 per cent annually, while paid profile conversion is about 23-24 per cent. The company has 700,000 paid users, of which 60 per cent are new users, while the rest are payments for renewal of services. Average transaction value has increased by 7.5 per cent year-on-year (y-o-y) to Rs 4,242 in the June quarter and could inch up further, both on price hikes as well as cross-selling of services.

Going ahead, while revenues have grown at 12 per cent annually over the past five years, it is the scale effect, which is expected to percolate to the operating and net level. The company’s operating profit margins, which has been in single-digits before FY17, hit the 23.3 per cent mark in the June quarter and was 20 per cent in FY17. Given that the segment profitability of the matchmaking business is over 30 per cent, lower operating cost in terms employees and shutting down of unprofitable operations is expected to further improve margins and bottom line. Part of the improvement in operating performance will come about as Rs 130 crore of the Rs 500 crore will come to the company (the rest is offer for sale) and will help repay overdraft facility of Rs 43 crore and to set up a corporate office in Chennai at Rs 42 crore. The company is also investing in brand awareness to the tune of Rs 20 crore to grow its market share and online user base.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

₹249

Renews automatically

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in