"More gains for Vedanta, some positives for Cairn as well")

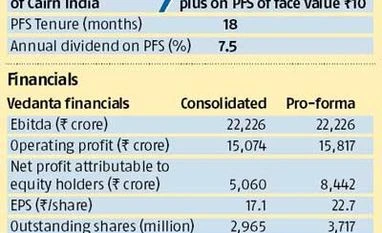

The buzz on the Street for the Cairn India-Vedanta merger came true with the formal announcement on Sunday. While the swap ratio at 1:1 was in line with the guesstimates doing the rounds, Vedanta will also be issuing Cairn’s minority shareholders one 7.5 per cent redeemable preference share (face value Rs 10) in the company for every share held in Cairn. Although this takes the effective swap ratio to 1:1.04, the preference share issue is mainly to prevent the Vedanta, (the Britain-based parent of Vedanta) shareholding from falling below 50.1 per cent.

While Piyush Jain of Morningstar feels there is more likelihood now of Vedanta getting a nod from minority shareholders, given the fair value of Cairn India (as estimated by other analysts) it might still not be enough.

The fair value of Cairn India, after discounting for the Rs 20,500-crore tax demand, comes to Rs 250-275 a share, say analysts. While the jury is out, let's see how the deal works out for the shareholders.

Though it is being argued that the merger accrues more positives for Vedanta, it will also be beneficial for Cairn India, looking at the uncertainties. There is a pending tax demand being contested by Cairn (as well as Vedanta); after the merger, this will become a contingent liability for the merged entity.

In short, in case the tax liability materialises, which for a standalone Cairn could wipe out its entire cash balance, after the merger it would be borne by a much bigger balance sheet. The low crude oil prices that impacted Cairn’s profitability are also not likely to move up in a hurry. Analysts at Barclays are factoring in a Brent crude oil price (per barrel) of $65.3 and $82.5 in FY16 and FY17, respectively, and $90 thereafter till FY20 in their estimates for Cairn India.

The Street is also concerned about Cairn’s stagnant production. The company, though, believes production after being flat in the near term will rise.

A combined entity, with better financial performance and improved credit ratings, is expected to benefit Cairn India shareholders, too. They’d also see de-risking in terms of business exposure. After the restructure, Macquarie’s target price for Vedanta is Rs 276.

While some experts argue Vedanta is gaining from the current cheap valuations for Cairn, its valuations are also down due to the weak base metal prices. However, the merger will give it full access to Rs 18,000 crore in Cairn India’s books.

While Piyush Jain of Morningstar feels there is more likelihood now of Vedanta getting a nod from minority shareholders, given the fair value of Cairn India (as estimated by other analysts) it might still not be enough.

The fair value of Cairn India, after discounting for the Rs 20,500-crore tax demand, comes to Rs 250-275 a share, say analysts. While the jury is out, let's see how the deal works out for the shareholders.

Though it is being argued that the merger accrues more positives for Vedanta, it will also be beneficial for Cairn India, looking at the uncertainties. There is a pending tax demand being contested by Cairn (as well as Vedanta); after the merger, this will become a contingent liability for the merged entity.

In short, in case the tax liability materialises, which for a standalone Cairn could wipe out its entire cash balance, after the merger it would be borne by a much bigger balance sheet. The low crude oil prices that impacted Cairn’s profitability are also not likely to move up in a hurry. Analysts at Barclays are factoring in a Brent crude oil price (per barrel) of $65.3 and $82.5 in FY16 and FY17, respectively, and $90 thereafter till FY20 in their estimates for Cairn India.

The Street is also concerned about Cairn’s stagnant production. The company, though, believes production after being flat in the near term will rise.

A combined entity, with better financial performance and improved credit ratings, is expected to benefit Cairn India shareholders, too. They’d also see de-risking in terms of business exposure. After the restructure, Macquarie’s target price for Vedanta is Rs 276.

While some experts argue Vedanta is gaining from the current cheap valuations for Cairn, its valuations are also down due to the weak base metal prices. However, the merger will give it full access to Rs 18,000 crore in Cairn India’s books.

Analysts at UBS also say that Vedanta has upcoming debt maturities of $2.4 billion by the end of FY16 and $3.3 billion by FY17. Even if these are not going to be paid down via cash, refinancing might be more forthcoming if Vedanta has control of cash-generating Cairn India.

Additionally, Vedanta on a standalone basis was estimated to generate an Ebitda (earnings before interest, taxes, depreciation and amortisation) of Rs 7,388 crore during FY16.

Of this, Rs 6,785 crore was to go in interest payment and Rs 116 crore in tax. Thus, profits would have been only Rs 466 crore, says Macquarie. On the other hand, the estimated Ebitda of the merged entity (standalone basis, excluding Hindustan Zinc) will be Rs 13,416 crore. With net debt reducing from Rs 60,830 crore to Rs 41,178 crore, interest outgo also reduces by a third and profits to be nine-fold higher.

The merger is subject to minority shareholders’ nod and regulatory clearances. Kotak Institutional Equities’ analysts said “A merger might involve the transfer of petroleum mining rights, as well as production sharing contracts for the Rajasthan and other domestic exploration and production blocks, which will require consent from the government and joint venture partner, ONGC.” This could take time, looking at the tax demands.

For Cairn India shareholders, though, the loss would be that they will no more be a part of a pure oil-play. Second, from owning shares of a cash-rich firm (worth Rs 130 a share), they will own shares of a company with leverage on its books.

However, Axis Capital said: “We expect Vedanta to rerate, as Cairn merger provides immense financial flexibility due to access to Cairn’s $2.7-billion cash reserves and annual Ebitda of $1 billion (even at $65 crude oil price). The merger will also unfold the true potential of Cairn, which always had a valuation overhang due to an impending amalgamation with the parent. Cairn shareholders will also gain from diversified earnings stream and rerating of Vedanta stock. Vedanta’s weightage in key indices will increase due to a larger equity base and reduction in promoter holding (50.1 per cent versus 62.9 per cent). Vedanta’s weightage in BSE will likely go up to 1.5 per cent versus 0.9 per cent currently.”