"Morgan Stanley believes SBI is well-placed to capitalise cyclical lift")

The rally in State Bank of India’s (SBI’s) stock may have gotten another leg with global brokerage Morgan Stanley raising its one-year target price to Rs 600 apiece. In their bull-case, the target price is pegged at Rs 830, implying a 100 per cent upside from Wednesday’s close.

“SBI has built a strong retail franchise and also sustained its deposit market share. Even on digitization, the progress has surprised, unlike other state-owned banks. As the corporate cycle turns, we expect earnings estimate upgrades and significant re-rating,” it said in its report dated February 17.

The shares hit a fresh lifetime high of Rs 426 on the BSE, up 3.5 per cent in the intra-day trade today. The stock has zoomed 50 per cent so far in the current calendar year, and 46 per cent alone in the month of February. In comparison, the S&P BSE Sensex and Bankex index have gained 8.2 per cent and 16.1 per cent, respectively so far in CY21.

The rally, Morgan Stanley believes, could continue as SBI has a much better balance sheet and profitability, and is well placed to improve earnings as the cycle turns. Against this backdrop, the stock could re-rate sharply and present significant upside, it said.

Factors behind price target hike:

Improved macro-economy: Drawing parallels with the economic growth clocked by India in early 2000s, analysts at the brokerage that India is at an inflection point that marks the start of a new virtuous growth cycle. Led by accommodative monetary policy and supportive fiscal policy; favourable external demand; and likely recovery in private capex in the next 12 months Morgan Stanley believes India could log gross domestic product (GDP) growth of 12.1 per cent in FY22 (up from previous estimate of 10.1 per cent), and of 6.7 per cent in FY23 (up from 6.2 per cent).

"In early 2000s, when the economy recovered, SoE banks registered significant outperformance in the initial years. Therefore, SBI could gain significantly as it is better placed than other PSBs in terms of profitability and capitalization,” the report said.

Strong retail loan growth: MS notes that retail loans now contribute 35 per cent of overall loans compared with 20 per cent five years back. The share of relatively less risky loans has also moved up.

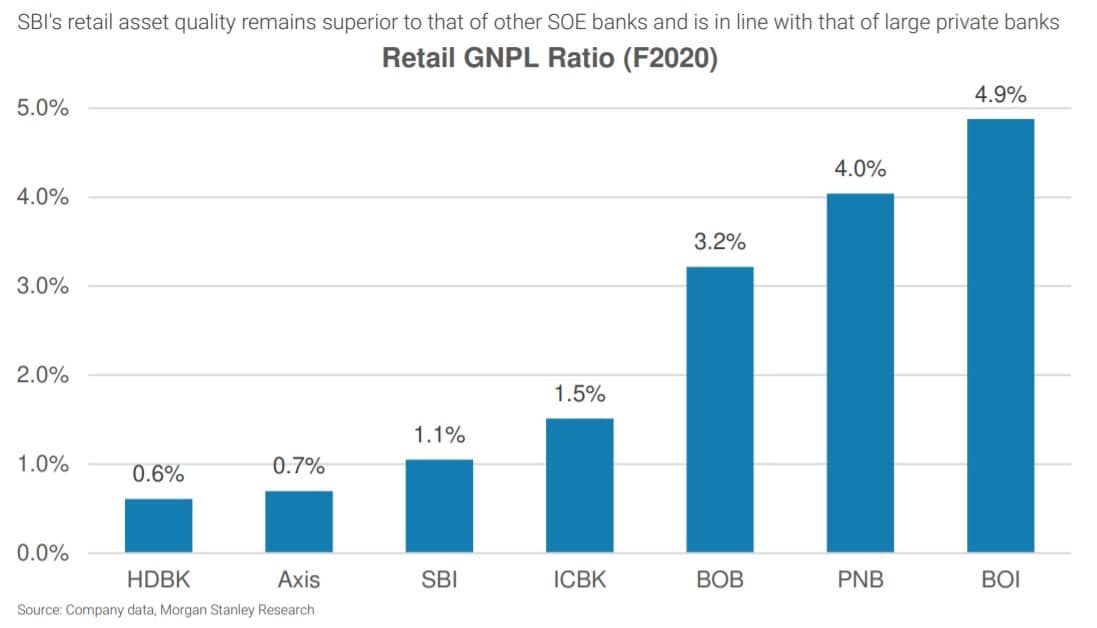

That apart, SBI's retail asset quality remains superior to other SOE banks and is in line with that of large private banks. At the end of FY20, SBI’s gross non-performing assets (GNPA) ratio in the retail segment was 1.1 per cent, lowest among PSBs, and third in the entire banking space. CLICK HERE FOR THE CHART

{kind=link}

Focus on digitization: SBI, the brokerage says, has maintained its market share (in terms of deposits and digital parameters) despite asset quality pressures over the past five years. Registered users on its YONO app have jumped from 7.3 million in Q4FY19 to nearly 33 million in Q3FY21. Moreover, its online market place gross merchandise value (GMV) has increased from Rs 50 crore in Q1FY21 to Rs 230 crore in Q3FY21. CLICK HERE FOR THE CHART

{kind=link}

Sustained deposit market share: “SBI has ensured sustained deposit market share relative to SoE bank peers – we see strong potential for SBI to accelerate current account market share gains as the revised guidelines by the RBI are put in place,” the report said. CLICK HERE FOR THE CHART

{kind=link}

Investment rationale

As the economic cycle gets stronger, banks generally tend to surprise positively on the earnings cycle supported by lower provisions and higher operating profit margin. “SBI is well placed to reach over 1 per cent return on asset (RoA) in F22/F23 in our bull case,” say analysts at the brokerage.

On the asset quality front, Morgan Stanley notes that SBI has done well in the retail segment by focusing on secured loans (which make up two-thirds of retail loans), and on unsecured lending (mainly to government employees or strong companies).

“Consequently, we believe that SBI's corporate/retail loan book, which is 65 per cent of overall loans, has the potential to surprise positively over the next two years,” it added.

As regards operating profit margin, MS opines that SBI has a significant amount of excess liquidity with loan-deposit ratio at close to 60 per cent which should allow it to generate loan growth of 10-12 per cent over the next 2-3 years.

“We believe interest rates have bottomed and as they move higher, margins will benefit. This will also be reflected in corporate banking, where disintermediation by bond markets increases as rates move lower, and hence corporate spreads come under pressure. In our bull case, we expect margins to rise ~10bps higher than in our base case,” it said.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in