"NCDEX plans for commodity derivatives to address NPAs, volatile agri prices")

Vijay Kumar V, managing director & CEO, National Commodity & Derivatives Exchange Limited (NCDEX), plans to make commodity derivatives, more importantly options, a tool to address non-performing assets (NPA) and volatile agriculture crop prices.

He told banks, market participants and farmer organisations to use commodity options similar to an insurance policy and hedge their positions by locking minimum profits.

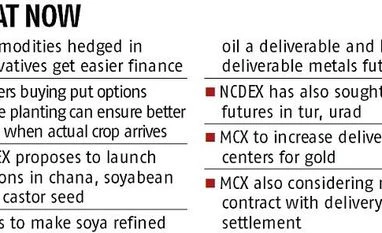

NCDEX will propose to the regulator to allow options in more agri commodities like chana, soyabean and castor seed, among others, as underlying futures in these commodities are fairly liquid.

It also proposes to make soya refined oil a deliverable contract and launch deliverable metals futures.

The cost of buying option is minimal but if the price direction goes against what has been anticipated, then the option will help in capping the profit and protect farmers from falling prices.

Kumar said that in the first ever media interview after taking over as MD & CEO in January that, “finance and commodity markets are gradually converging. Option market in commodities is gaining momentum and farmer organisations can make use of this tool to lock minimum profit. Banks can also secure their lending risks by seeking hedge details in futures or options from borrowers.”

Banks can ask their borrowers to hedge the price volatility risk of raw materials or commodities against which they have taken loans in futures market, and in options, if available. Even farmers can sell a part of their crop, estimated at the time of sowing, to ensure they get the price they intend to get even when it falls at the time of crop arrival. Farmers can buy put options of the crop they have sown.

Even bank borrowers can buy put for the commodity which they have pledged to get a loan. The Reserve Bank of India (RBI) has already told banks to ask their borrowers to hedge their commodity price risk on commodity exchanges. Now, bank's commodity broking subsidiaries are taking membership of the comexes. Kumar said, “We have proposed broking subsidiaries of banks suggesting them to make wider use of commodity futures & option platform.”

For example, if a loan is taken against guar seeds by a borrower of a bank, he can buy put option of guar seed from a bank broking subsidiary. If prices fall, he has to increase collateral for borrowing in general practice. But now, they have more efficient tool ‘Options’. So, when the price falls, put option premium goes up which can be adjusted for marking borrowing to market rate and he saves paying additional collateral. Bank can charge less collateral or reduce interest rate for such hedged stock when pledged as mark to marker risk is lower. This also help banks reduce asset turning non-performing. Options here works as an insurance policy.

Anuj Gupta, Deputy Vice presidents, commodities and currency research, Angel Broking, said, “Usually, at the time of arrival, we generally witness a sharp decline in prices and during scarcity of the commodity we noticed an appreciation in prices. During sharp movement in prices at the time of arrival and scarcity, one can use options. We have also noticed that few commodity are still trading below its MSP like pulses, guarseed and oilseeds.” He also said, “At the time of arrival, if prices are going down, then farmers may use Put option of that particular commodity to prevent it from the falling prices. It is just like an insurance of the prices of the crop.” However, to see that happening, there is a need for an enlarged list of commodities available for options in agri segment and that should be liquid.

Commodity derivatives have other benefits too. Sanjay Kaul – MD & CEO – National Collateral Management Services, indicated that taking finance using commodities as collateral will be beneficial to the borrower also if the same commodity is hedged in derivatives either in futures or in the option segment. He said, “hedged contracts have minimal price risk and higher loan to value is safe for financiers also. Hence, lower collateral and lower margins are required in such cases.”

Even MCX, India’s largest commodity exchange is making brass metal futures market friendly and will later introduce a few deliverable metal contracts. It is also expanding the delivery centres for gold contract. At present, only Ahmedabad is the delivery centre and is adding New Delhi, Kolkata, Mumbai, Kochi, Chennai and Hyderabad to the list of delivery centres.

Even MCX has seen good traction in its cotton futures contract with record 161,000 bales delivered in the July contract which suggest good hedging. MCX is also helping farmers or their association-bodies or farmers’ producers organisations by connecting them to convert Kapas (raw cotton) in cotton bales.

Currently, Sebi norms suggest that when the option expires, if it has not been carried forward to the next contract or not squared off, then the option devolves in futures and then all rules regarding futures are applicable, including margins to option holders as position becomes a futures position.

However, Kumar said, “We have proposed appropriate changes to the market regulator to make options more market friendly. This will help the option seller who is willing to give delivery and smoothen the process. For giving delivery, he will comply with all norms and does not have to hold futures positions on option expiry and still wait for staggered delivery period. This way, the option becomes a virtual insurance policy and the option premium is like policy premium.”

Even commodity processors can sell put options. If price rise when they actually buy the produce, price of the option that they have sold will give them profit and reduce actual procurement cost.

The government has vested the Sebi with powers to decide listing and delisting commodities for derivatives from the list of 91 notified ones. Following this, NCDEX has proposed to the Sebi to relaunch tur and urad futures which were suspended in 2007. “This makes pulses complex comprehensive for market players,” said Kumar.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in