"New India IPO is reasonably valued: Should you invest now?")

It’s a rain of Initial Public Offers of equity (IPOs) at D-Street and keeping pace with its target, New India Assurance (NIA) is to launch its offer on Wednesday. In the general insurance sector, it enjoys the status that State Bank of India or Life Insurance Corporation have in those segments, respectively.

NIA has comfortably maintained its first position across key parameters such as net worth, gross domestic premium and branch strength. And in major product categories. These factors and reasonable valuations (30 times the FY17 price to earnings) support the offer. Retail (small) investors also get a discount of Rs 30 a share.

Business

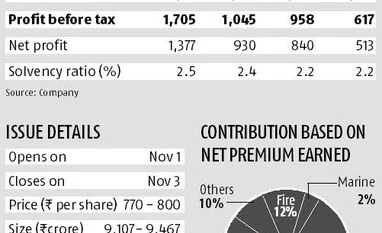

A big chunk of NIA’s business is derived from two products in the general insurance space, motor and health (see chart). It has 15 per cent and 18 per cent share, respectively, in these, the top spot. NIA also holds leadership position in the marine and fire insurance segments, though their contribution is relatively small to the revenue.

Financials

More From This Section

While NIA had the highest gross direct premium and net worth in the sector, of Rs 19,115 crore and Rs 12,090 crore, respectively, in FY17, the overall financials have lately been shaky. In FY16 and FY17, operating loss was Rs 901 crore and Rs 533 crore, respectively. This was mainly on account of having to provide for higher loss ratios in the health and motor insurance segments.

However, with recent price increases implemented for pockets such as retail health policies, the impact of this blip is expected to even out in FY18 and improve notably from FY19. In the June 2017 quarter (Q1), operating profit was Rs 178 crore, showing the impact of price hikes.

Valuation

Priced at Rs 770-800 a sharepiece, the IPO is valued at 30 times the FY17 price to earnings (PE) ratio. Extrapolating the Q1 results, the PE for FY18 is about 28 times, a reasonable discount to ICICI Lombard’s FY18 asking rate of 40 times. While one could argue that the latter is relatively stronger in profitability, at Rs 513 crore of net profit in Q1 and a higher return ratio (return on equity), NIA is over twice the size. If net worth is considered, including fair value change account, NIA’s business is five times larger than ICICI Lombard, indicating that the lower valuations also factor in the relatively subdued financial performance.

Risk

NIA hasn’t done price hikes across all products. Group health insurance and a few categories of motor insurance are laggards, where it is expected to do this in the coming quarters. Any delay in this could defer profitable business growth by another financial year.