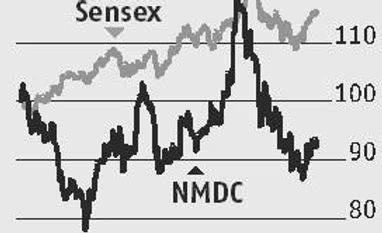

"NMDC: Steady steel demand, increasing iron ore volumes key growth drivers")

NMDC, the country’s largest iron ore producer, had to cut the price of its produce by Rs 100 a tonne from April 18, due to decline in international prices. The per tonne iron ore price, excluding China, has corrected from over $75 levels in end-February to sub-$65 by start of April on fears that the global tariff wars would impact steel and iron ore demands.

China’s steel demand was also seen to be a bit weak. Consequently, NMDC, which had seen continued rise in prices of iron ore lumps and fines (up 34 per cent and 38 per cent respectively since November 2017), had to cut it by 3-4 per cent in March and by another 3-4 per cent from 18 April to Rs 2,900 for lumps and Rs 2,560 for fines.

While the price cuts will affect its revenue and profits, and thereby leave their impact on the street sentiment, the correction is an opportunity for long-term investors, observe analysts. The steel demand in India continues to grow and is expected to increase by 5 per cent in FY19. Similarly, the demand for iron ore is also likely to remain strong.

More importantly, NMDC is increasing its mining capacity, which will help sustain growth. NMDC proposes to augment its iron ore production capacity in phases to 67 million tonnes per annum (mtpa) by FY22 from 34.05 mtpa in FY17. The removal of produce has improved too. In the March quarter, analysts at Kotak Institutional Equities estimated NMDC's iron ore sales to rise by 8 per cent year-on-year to 10.5 MT (up 31 per cent sequentially). Further, NMDC, with its long-term mining leases, is already expected to benefit as a number of private mining leases will expire by end of FY20.

For the March 2018 quarter, analysts at Motilal Oswal Securities estimate NMDC’s Ebitda to increase by 54 per cent sequentially to Rs 20.4 billion, led by higher iron ore prices and a recovery in volumes as the rail infrastructure issue (easing transportation hurdles) has been resolved. Their target price of Rs 225 indicates a significant upside from the current levels of Rs 124, as they believe valuations are ignoring the value of its steel plant.

HDFC Securities, too, had recommended investors to add the stock on dips around Rs 119-123, indicating an enterprise to Ebitda valuation of 4.5x based on FY20 estimates, for targets ofRs 163 over next few quarters. In addition, investors can also look forward to a 4-5 per cent dividend yield.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in