"Pharma growth to pick up in 2nd half")

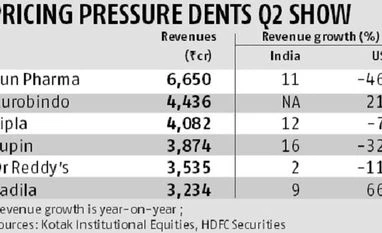

Expectations of a gradual reduction in pricing pressure in the US market were belied as Indian pharmaceutical companies reported another quarter of muted growth. On the back of 11-12 per cent price erosion in the US market, year on year, revenues of the top generic pharma companies fell a little over 20 per cent over the year-ago quarter. The brokerages had expected some pricing pressure but the results indicate this was as severe as in the June quarter.

Barring Cadila Healthcare and Aurobindo most Indian pharma majors revenue from the US market fell, by seven to up to 46 per cent. This country accounts for a little over 30 per cent of sales. One reason for the fall has been a sharp increase in product approvals, both for existing generic products and for drugs under the sale exclusivity period. For example, Lupin’s sales in the US were down 32 per cent over a year on loss of exclusivity for Minastrin (a contraceptive) and pricing pressure in anti-diabetic medications Glumetza and Fortamet.

Similarly, Sun Pharmaceutical industries reported a 44 per cent fall in US revenue on account of a pricing pressure on the base business (dermatology portfolio), deferring in sales of some products to the December quarter and falling contribution from the generic of cancer drug Gleevec. The company had enjoyed marketing exclusivity for this drug in the year-ago quarter.

What has been pegging back US revenue, in addition to increased competitive levels, are the lack of approvals due to regulatory issues. Analysts believe the lack of approvals for Sun Pharma (Halol) and Dr Reddy’s (Srikakulam, Visakhapatnam) has been due to facilities not compliant with the US regulations. Most companies in the US market neither have the volume or the new product levers to counter price erosion on account of generic launches, as well as consolidation of the distributor chains.

The outliers among larger companies have been Aurobindo Pharma and Cadila Healthcare. They reported 17 per cent and 37 per cent growth, respectively, in overall sales, on the back of limited competition products.

Most companies have been cautious about growth for 2017-18. Sun Pharma has maintained it expects single-digit revenue decline for FY18 on a consolidated basis; analysts believe a large part of this is on account of the disappointing US performance. Analysts at ICICI Securities expect the company’s US sales to fall by 24.7 per cent, due to delay in product approvals and continued pricing pressure. On profitability, the management has indicated a margin of 20-22 per cent, much lower than the 30 per cent it was reporting after the Ranbaxy integration.

The positive for the sector has been the expectation from most managements that the second half of FY18 would be better than the first half. This is because the June quarter was one of the weakest reported by Indian drug companies in recent times, a weak US market being compounded by Goods and Services Tax disruption in India and currency-related issues in other markets. This had impacted revenues and shrunk margins of all players.

Further, analysts at Kotak Institutional Equities expect launches to pick up from the second half of FY19, driving US generic revenue and overall revenue and profit.

On a sequential basis, growth seems to have picked up in India, second most important market by revenue for the larger drug makers. After declining by two to 10 per cent in the June quarter, companies reported double-digit growth in domestic sales. Cipla, Lupin and Sun Pharma reported 11-16 per cent year on year growth, on the back of channel restocking, helping offset some of the pain in the US market.

Analysts, however, say it will take some more quarters for sales to come back completely, as secondary sales data indicate there is still inventory in the channel. Ranvir Singh of Systematix expects domestic industry growth to come back to 10-12 per cent levels on an annual basis.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in