Price rise to boost Coal India profitability

Street cautious due to lower realisations in September quarter but benefits should start flowing in second half of FY14

Ujjval Jauhari Mumbai

The news flow for Coal India over the past week has been mixed. While the news of the Competition Commission of India slapping a Rs 1,773-crore penalty has been a dampener, the company’s decision to effect a price rise is a positive. Analysts don’t see the fine as a setback, as the company will contest the case and the penalty is only three per cent of the cash reserves.

Even if the company has to pay, the impact is estimated at Rs 3 a share.

The raising of the price of non-coking coal from its Western Coalfields holds significance. This source produces 44-45 million tonnes or about eight per cent of the total produce. With the notification of a 10 per cent rise, the company also raised its rapid loading charge and non-coking coal sizing charge by 15-60 per cent, depending on size. With this, it expects to earn incremental revenue of Rs 197 crore during FY14. On an annualised basis, analysts at Prabhudas Lilladher expect Rs 1,200 crore of incremental revenue or a Rs 23 a tonne rise in prices.

Abhisar Jain at Centrum Broking expects the decision to boost earnings before interest, taxes, depreciation and amortisation (Ebitda) by Rs 10-15 a tonne. He sees the blended realisations improving by two per cent from these measures.

Investors cautious While the price rises bodes well, the Street will be looking at performance in the coming quarters. The caution is due to the weak realisations during the September quarter, despite the price increase of five to six per cent in May for coal supplied under fuel supply agreement (FSAs) to power projects. Also, the dispatches of 109 mt during the quarter were 7.3 per cent higher over a year earlier. Analysts attributed this to the lower grade of inventory liquidated by the company, leading to a dip in realisations.

Further due to FSA commitments, coal supply to power projects was sharply higher, whereas offtake to non-power customers (particularly cement and sponge iron projects, where the yield is much more) was lower. The e-auction prices were also lower, due to weak international prices and lower industrial activity.

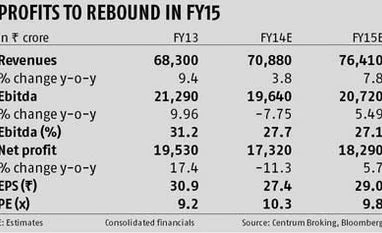

Profitability, dividend & valuations Nevertheless, analysts expect the second half to be better. Prabhudas Lilladher expects CIL’s e-auction volumes to grow 50-55 per centover a year in the December quarter, more than offsetting the 25 per cent fall in realisation. This should put to rest the Street’s concern on volumes and earnings in e-auctions.

Over the longer term, though, volumes will increase and better realisations bode well. Nevertheless, on the flip side, analysts expect the benefits of FSA incentives to not accrue to the company from FY15. Jain has, for thee new FSAs of 71 Gw being signed, removed the benefit of incentives completely from FY15. While he maintains volumes of 484 mt and 508 mt in FY14 and FY15, respectively, he has revised the Ebitda for both upwards, by 2.1 per cent and 4.2 per cent, respectively.

Reports suggest the company has also pushed the special dividend decision to February 2014, while the government might not go for divestment of stake due to protests by workers. This, if it happens, will remove a major overhang on the stock, while the expected dividend, pegged at Rs 25-30 a share, will be good for investors.

Of the 16 analysts polled in December, 10 have ‘buy’ ratings, five of ‘hold’ and one of ‘sell’, with a consensus target price of Rs 328, according to Bloomberg. The stock is trading at Rs 283.20.

"Price rise to boost Coal India profitability")