"Pricing and margin worry may downgrade UltraTech Cement; stock falls 1.5%")

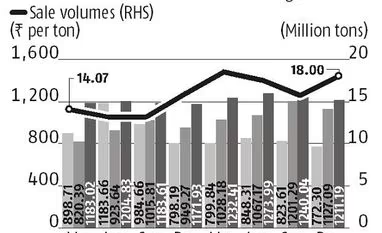

UltraTech Cement reported better- than-expected growth in revenue for the December quarter, with net sales growing 18 per cent over a year to Rs 8,812 crore. Analysts had estimated Rs 8,641 crore.

The surprise was better realisation, year-on-year. While sales volume grew 14 per cent to 18 million tonnes (mt), in line with Street expectations, sales realisation rose 4 per cent. This was due to a 15 per cent rise in volume from the trade segment, where pricing is higher.

The segment accounted for 64 per cent of total sales volume in the quarter.

However, pricing remains a near-term overhang for the entire cement sector and this could weigh on the market leader’s earnings. Though the management pointed to an improvement in pricing in some parts of the country in January, and even in the competitive non-trade segment, this might not hold in the near term with the coming general election. Analysts are expected to downgrade net profit estimates, amid pricing concern and margin pressure.

What could help offset some of the pressure could be cost saving with the sharp correction in crude oil prices and improvement in the rupee-dollar exchange rate. The management indicated there would be benefits here from the March quarter.

Prices of key inputs such as petcoke (35 per cent of the requirement is imported) have gone down after the crude oil price correction. Petcoke is 70 per cent of the company’s fuel mix.

For 10-12 per cent less in petcoke price, there could be a two per cent saving in total cost, says the management. Also, a five to six per cent fall in the price of diesel, which impacts freight cost, could save 1.5 per cent in the total cost.

In the quarter, however, there was a 121 basis points fall from a year before in Ebitda (earnings before interest, tax, depreciation and amortisation, excluding other income) margin to 15.8 per cent. This was due to an 18.7 per cent year-on-year surge in power and fuel cost per tonne of selling volume, and a little over three per cent rise in freight cost. Petcoke cost was up 11 per cent. Thus, the Editda per tonne was lower by three per cent, to Rs 772. This dragged down the net profit, which rose 6.5 per cent over a year before to Rs 449 crore.

As the Street estimate was for Rs 500 crore, this hurt investor sentiment and the share price was down 1.5 per cent on Thursday to Rs 3,790.

The recent acquisitions such as Jaypee, erstwhile Binani and Century, among others, and its pan-India presence improves the leadership position of UltraTech. Analysts believe the sharp capacity augmentation would help propel volumes in the long term, despite the management’s concern over near-term demand.

Also, there would not be significant cost addition required for ramping up the assets acquired from Century Cement.

(With inputs from Amritha Pillay)

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in