"Relying on unsecured products to drive profitability is risky: Analysts")

A cursory reading of the Reserve Bank of India’s (RBI’s) loan growth data for January 2019 appears strong and positive. With 13 per cent year-on-year system growth and green shoots in lending towards industries (up 5 per cent), this appears to be a better period in recent times.

But below the surface, problems remain. While the segment continued to grow at 17 per cent year-on-year in January 2019, mirroring the trend in the past 5-6 months, the growing relevance of unsecured loans was unhealthy.

Analysts at Kotak Institutional Equities note that frontline banks are focusing more on unsecured products to drive profitability and it is a risky strategy.

A dissection of retail loan data indicates that while the share of home loans, including priority sector housing loans, remains at over 50 per cent of retail loans, the share of unsecured loans categories such as credit cards and personal loans, which aren’t asset-backed, have gone up from 29 per cent a year ago to 32 per cent in January 2019. Faster growth in the segment doesn’t provide comfort because retail loans is a space where private banks hold higher market share.

Results for the December quarter (Q3) also revealed that top private banks posted ahead of average growth in unsecured products. For instance, the market leader, HDFC Bank, posted 24 per cent growth in overall retail loans, while its credit cards and personal loans business grew faster by 33 per cent.

The share of these unsecured businesses rose from 16 per cent a year ago to 17 per cent in Q3 and on a longer term, their share has risen from 10 per cent in FY14. A similar trend is visible across private banks (see table).

Analysts at Ambit Capital, who have a ‘sell’ rating on HDFC Bank, observe that the primary reason for an increase in risk-weighted assets to total assets from 27 per cent in FY16 to 35 per cent as of September 2018 seems to be the increasing share of unsecured loans. While peers too have seen a sharp increase in the proportion of unsecured loans to overall retail loans, at 17 per cent of retails, HDFC Bank’s share is higher compared to its immediate peers (see chart). Analysts at Kotak Institutional Equities stress that the rising contribution of the unsecured loan mix to overall earnings is a key risk for the bank.

While the risk is looming, investors don’t have to be alarmed just yet. For one, Vineeta Sharma, head of research at Narnolia Financial Advisors opines that with credit bureaus working effectively, it reduces the risk of asset quality compared to the past instances like the one in 2008-09. “Despite asset quality deteriorating a bit, I don’t see major concerns in the segment now,” she affirms.

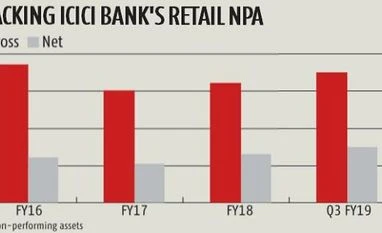

Her faith is reflected in the non-performing asset (NPA) trends published by ICICI Bank. While in absolute terms, retail NPAs are on the rise, when seen as a percentage of loan book, their NPA levels are well below the FY16 threshold, despite some quarterly variations (see table).

That said, Rakesh Sharma of Elara Capital feels close monitoring on these assets is required. “When the overall economic trend is strong, cycle for retail NPAs get stretched a bit. But the first signs of asset quality pain is a slowdown in unsecured loans followed by rising NPAs in the segment,” he adds.

This is why analysts believe the next two-three quarters would be crucial to gauge the health of these unsecured retail loans.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in