"Rising yields, exposure to IL&FS' shrinking returns hit debt funds")

Debt funds have had a poor run over the past year with the spike in yields and some schemes' exposure to IL&FS’ shrinking returns.

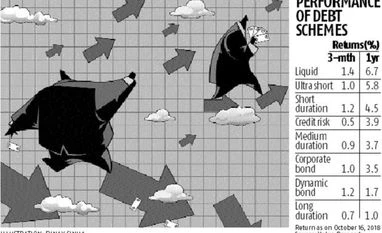

Liquid and ultra-short term funds emerged the top performers, with one-year returns of 6.7 per cent and 5.8 per cent, respectively. Dynamic and long duration funds, on the other hand, were at bottom of the pile, with returns of 1.7 per cent and 1 per cent, respectively, shows data collated from Value Research.

“The biggest factor has been duration; funds with the least duration have done reasonably well whereas long-duration funds have suffered from the spike in yields," said Vidya Bala, head of mutual fund research at FundsIndia.

Bond prices and yields are inversely proportional - as prices increase, yields fall. The Reserve Bank of India (RBI) has increased rates by 50 basis points in the past one year.

The RBI opted to maintain status quo in its policy meeting on October 5, which has brought some relief on the interest rate front.

"Given the status quo, we expect short-term rates to ease while long-term yields may trade range bound. The macro needs monitoring, and rupee and crude oil prices could lead the way for markets going forward," Lakshmi Iyer, CIO (debt), Kotak Mahindra Asset Management, had said in a note after the policy decision.

Yields of 10-year government papers have surged 115 basis points to 7.91 per cent, from 6.76 per cent a year ago.

The exposure to IL&FS, on the other hand, had a greater impact on the shorter tenure funds. Some fund houses had taken significant exposure to debt papers issued by IL&FS and its subsidiaries. These schemes had to take a sharp haircut on their exposure, following the multi-notch downgrade of parent IL&FS. As these markdowns impacted net asset values of the schemes, investor returns were also hit.

The tight liquidity environment made it difficult for MFs to offload commercial papers of duration as low as one or two days. Some large fund houses even borrowed from banks to meet the incremental redemption requests last month.

Total assets under management of the MF industry shrunk to Rs 22 trillion in September Rs 25.2 trillion at the end of August. Most of the damage was due to record outflows from liquid and fixed income schemes, in which large investors invested. The two categories saw outflows of Rs 2.4 trillion in September - the most since at least January 2008.

In addition to the quarterly phenomenon of high redemption related to advance tax payments, the tightness in money markets and continuous rise in yields also added to outflows, according to ICRA.

“The losses for accrual funds are mark to market. As long as investors hold their short term debt schemes for the duration for which they entered, they will not lose out. Long term funds, however, will continue to remain under pressure unless the interest rate cycle turns,” said Bala.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in