"Street sees re-rating potential in Dabur's stock")

Firstly, the company expects the current volume growth to be maintained, which is a big positive amid the challenging scenario fast-moving consumer goods (FMCG) companies are facing. This will be aided by recovery in the Namaste business, improving distribution reach and investment in new products. Secondly, margins are also likely to inch up due to the above factors further aided by benign raw material prices and stable ad spends. Lastly, valuations too, are reasonable.

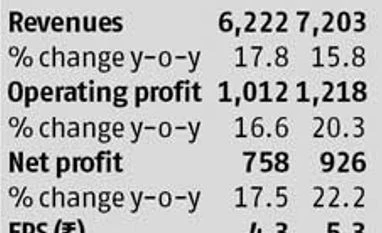

At Rs 142, the stock trades at 27 times FY14 estimated earnings, which is one of the lowest among the FMCG players. Improving fundamentals along with reasonable valuations make the Dabur India stock an ideal re-rating candidate, believe analysts. According to Bloomberg, 68 per cent of the 44 analysts polled, have a buy rating on the stock. The most recent ones have a price target ranging Rs 140-167.

High volume growth to sustain

The company is cautious on the near-term outlook and thus conservatively expects to maintain the current level of volume growth of 10 per cent. Though it sees the possibilities of demand ebbing, especially for discretionary categories or higher value products, the same has not yet affected its portfolio which comparatively has few discretionary profile products. The company has also not seen any significant down-trading so far.

Latika Chopra, analyst, J P Morgan expects a steady volume growth of 8-10 per cent considering the company is focused largely on mass/mid-market portfolio.

"Dabur is likely to fare relatively better (vs peers) in a slowing consumption growth scenario, which is already affecting discretionary segments of staples adversely," she adds in her report dated March 18. Abhijeet Kundu, analyst, Antique Stock Broking, feels any surprises on volume growth could lead to a higher re-rating of the company and would be an (upside) risk to the target price assumptions.

Namaste to fare better

Analysts believe the worst is over for US-based Namaste, which Dabur acquired in late 2010. The business, which contributes about 10 per cent of consolidated revenues, should see gradual recovery starting FY14.

A meaningful impact of the current restructuring exercise though, will be visible only after a year. Dabur is working towards creating an efficient supply chain for Namaste in the African market, working on distribution restructuring and is undertaking brand re-launches for key products (recently, it did for ORS). It is also setting up manufacturing facilities in three destinations, namely West Asia, Nigeria and South Africa.

Other key initiatives

For the domestic business, the company plans to focus on rural markets (50-60 per cent of revenues) by increasing distribution reach and selling more profitable and low penetration products, strengthening its toothpaste portfolio by stressing on herbal-based and value-added positioning (like the recent launch of Babool salt) and sprucing up its hair care portfolio (focus on Almond hair oil, growing the Amla hair oil brand in South India and positioning shampoos on herbal platform). However, gains from these will need to be monitored as the said segments and markets are highly competitive.

While the company is taking steps to boost topline growth, stable raw material costs and relatively lesser need to spend on advertising and promotions should result in an uptick in margins, albeit marginally, in FY14. This is certainly positive given that many FMCG companies are facing pressure on the margin front.

The company gains strength from its well-diversified business wherein international business forms 30 per cent of consolidated revenues, oral care, hair care, health supplement and foods contribute another 50 per cent, while 20 per cent comes from a wide variety of products (digestives, home care, skincare, retail, etc).

Not having exposure to any single raw material (unlike many of its peers) helps in managing costs better. According to the management, advertising costs as a percentage to sales is also likely to continue to be around 14 per cent levels and there will not be any upward pressure on this front.