"Strong base, new buys to help maintain growth at Sun Pharma")

Sun Pharmaceutical Industries Ltd has been one of the outperformers in FY13, gaining 45 per cent, and in the process, breaking into the top 10 business groups by market capitalisation.

Its performance bests both its peer index, the BSE Healthcare, which gave 21 per cent returns, and the broader markets (BSE Sensex), which posted eight per cent gains. The stock has been hitting continuous highs recently as well on the back of price hikes and expectations of a strong March quarter.

The gains thus far have been the result of the company’s consistent performance in the US, both from Sun Pharma’s niche launches as well as its acquisitions—Taro, Dusa Pharma and URL. Its chronic-heavy India portfolio and its leadership in key therapies also ensure higher realisations.

These factors make it a favourite of pharma analysts. HSBC analysts, led by Girish Bakhru, are overweight on the company due to a resilient US business (current product portfolio) with a rich generic pipeline of 142 abbreviated new drug applications (ANDAs) pending approval, as well as consistently growing high-margin India business.

Analysts expect the company to post annual revenue growth of 20 per cent for the consolidated operations between FY12 and FY15, driven by its US operations (about half of consolidated revenues), which are likely to grow 25-30 per cent. Net profit growth during the same period is estimated at 19 per cent by analysts. The company is also sitting on cash and investments to the tune of $1 billion and is likely to look at small and medium size acquisitions.

All these positives mean that the company continues to trade at a steep premium (25 per cent) to the sector valuations and is available at the upper-end of its own historic one-year forward price-earnings (P/E) band. Most analysts (over 60 per cent, according to Bloomberg) have a ‘buy’ rating on the stock with the target price at about Rs 900, which offers little upside from the current level Rs 861. Hence, investors looking to buy the stock are advised to await corrections.

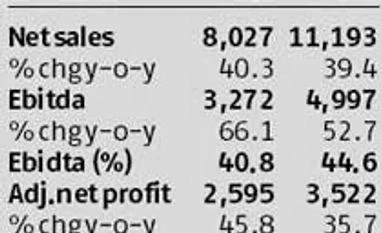

What has underlined Sun Pharma’s performance in recent quarters is the contribution of various companies within the group. “The combination of Sun Pharma and Taro offers an excellent business model for the company, as has been reflected in the 44 per cent year-on-year revenue growth and 48 per cent net profit growth for the nine months ended FY2013,” says a Sharekhan report. One of the reasons for this growth spurt has been Taro’s revenue jump over the last two years. Price increases in key products have helped achieve 27 per cent revenue growth in nine months ended December 2012. The bulk of the benefit of price increases has been flowing into earnings before interest, taxes, depreciation and amortisation (Ebitda) margins, which expanded from 30 per cent in FY11 to 59 per cent in the December 2012 quarter, says Chirag Talati of Espirito Santo Securities India.

Among the non-Taro portfolio, the company continues to ride on the sales of niche products, such as anti-cancer medicine Lipodex and Stalevo (to treat Parkinson’s disease). The consolidation of its US acquisitions, Dusa Pharma (acquired in November 2012) and generic business of URL (December 2012) should add to the US growth from the March quarter onwards.

The company has been able to stand out as a majority of its products falls in the niche areas, where it has not only become the leader, but has also been increasing its market share. Says Talati: “Sun Pharma’s differentiated approach in the domestic formulations market and the leadership position in super-specialty segments like central nervous system, cardiovascular system, diabetology and ophthalmology have ensured a superior profile of about 40 per cent Ebitda margin in FY12 as compared to its Indian peers.”

Given the market share gains, Espirito Santo Securities believes Sun Pharma could emerge as the second largest or the largest domestic formulations player over the next 12-18 months. Further, the research firm says growth for the market leaders, Abbott and Cipla, could moderate, given that they will be impacted more on account of the pharma pricing policy than Sun Pharma.

Its performance bests both its peer index, the BSE Healthcare, which gave 21 per cent returns, and the broader markets (BSE Sensex), which posted eight per cent gains. The stock has been hitting continuous highs recently as well on the back of price hikes and expectations of a strong March quarter.

The gains thus far have been the result of the company’s consistent performance in the US, both from Sun Pharma’s niche launches as well as its acquisitions—Taro, Dusa Pharma and URL. Its chronic-heavy India portfolio and its leadership in key therapies also ensure higher realisations.

These factors make it a favourite of pharma analysts. HSBC analysts, led by Girish Bakhru, are overweight on the company due to a resilient US business (current product portfolio) with a rich generic pipeline of 142 abbreviated new drug applications (ANDAs) pending approval, as well as consistently growing high-margin India business.

Analysts expect the company to post annual revenue growth of 20 per cent for the consolidated operations between FY12 and FY15, driven by its US operations (about half of consolidated revenues), which are likely to grow 25-30 per cent. Net profit growth during the same period is estimated at 19 per cent by analysts. The company is also sitting on cash and investments to the tune of $1 billion and is likely to look at small and medium size acquisitions.

All these positives mean that the company continues to trade at a steep premium (25 per cent) to the sector valuations and is available at the upper-end of its own historic one-year forward price-earnings (P/E) band. Most analysts (over 60 per cent, according to Bloomberg) have a ‘buy’ rating on the stock with the target price at about Rs 900, which offers little upside from the current level Rs 861. Hence, investors looking to buy the stock are advised to await corrections.

What has underlined Sun Pharma’s performance in recent quarters is the contribution of various companies within the group. “The combination of Sun Pharma and Taro offers an excellent business model for the company, as has been reflected in the 44 per cent year-on-year revenue growth and 48 per cent net profit growth for the nine months ended FY2013,” says a Sharekhan report. One of the reasons for this growth spurt has been Taro’s revenue jump over the last two years. Price increases in key products have helped achieve 27 per cent revenue growth in nine months ended December 2012. The bulk of the benefit of price increases has been flowing into earnings before interest, taxes, depreciation and amortisation (Ebitda) margins, which expanded from 30 per cent in FY11 to 59 per cent in the December 2012 quarter, says Chirag Talati of Espirito Santo Securities India.

Among the non-Taro portfolio, the company continues to ride on the sales of niche products, such as anti-cancer medicine Lipodex and Stalevo (to treat Parkinson’s disease). The consolidation of its US acquisitions, Dusa Pharma (acquired in November 2012) and generic business of URL (December 2012) should add to the US growth from the March quarter onwards.

The company has been able to stand out as a majority of its products falls in the niche areas, where it has not only become the leader, but has also been increasing its market share. Says Talati: “Sun Pharma’s differentiated approach in the domestic formulations market and the leadership position in super-specialty segments like central nervous system, cardiovascular system, diabetology and ophthalmology have ensured a superior profile of about 40 per cent Ebitda margin in FY12 as compared to its Indian peers.”

Given the market share gains, Espirito Santo Securities believes Sun Pharma could emerge as the second largest or the largest domestic formulations player over the next 12-18 months. Further, the research firm says growth for the market leaders, Abbott and Cipla, could moderate, given that they will be impacted more on account of the pharma pricing policy than Sun Pharma.