"Sustained improvement in businesses key to RCap's re-rating")

For one, the company has been witnessing operational improvement across all its key businesses. Take the case of Reliance General Insurance, which turned profitable in the December quarter (after four years). Easing regulatory overhang in the life and general insurance businesses will help improve growth and profitability further.

The company is also hopeful of bagging a banking licence and scale up its lending (NBFC) business.

The high-correlation of most of its businesses with the markets and the regulatory overhang are key concerns for the stock. Its NBFC business too, has not been able to scale up and is lagging peers in loan growth. Says Deven Choksey, managing director, KR Choksey Securities, “Reliance Capital's businesses are passing through their own specific challenges. Reliance Capital requires a better environment for a significant re-rating and the current price does not reflect its true valuations.”

However, analysts such as Kunal Shah are more positive on the stock. “RCap’s earnings have been volatile over the past few quarters due to stake sale and consolidation of group entities. The company’s core businesses of AMC and commercial financing have stabilised a tad or improved recently. Taking cognizance of its inherent value in life insurance and AMC businesses, coupled with scale up in consumer financing and stability in general insurance, we are positive on the stock”.

According to Bloomberg data, the consensus one-year target price for the scrip is Rs 520, translating into a significant upside from the current levels of Rs 308.

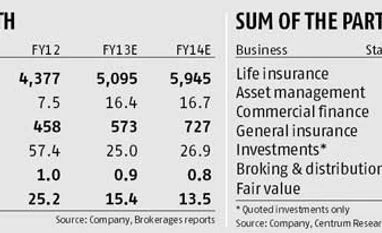

Meanwhile, among its key businesses, AMC’s revenues in the December quarter were boosted by Securities and Exchange Board of India’s (Sebi) new guidelines on income recognition (Sebi allowed flexibility to AMCs towards allocating their expenses, resulting in higher income via commission fees). However, its profit before tax (PBT) margins contracted from 45 per cent in the December 2011 quarter to 26 per cent in the December 2012 quarter, which is the lowest in the past four years due to change in accounting norms for AMC fees. While the management is expecting AMC and broking businesses to grow, their dependence on stock markets and tighter regulations will have a bearing.

But, the life, general and lending businesses are gaining traction. The life insurance business’ new business premium is likely to post 10-15 per cent growth (fell 35-45 per cent over the last two years), says the management. Notably, the company has moved away from ULIP business and traditional life insurance policies now form about 80 per cent of its product mix.

Lower combined ratio (claims and expenses divided by the premium earned), an expanded agent base and improving pricing enabled RCap's general insurance business return to profitability after four years. The company is now focusing on high-margin businesses such as commercial lines, fire and engineering insurance and plans to reduce its exposure to the motor segment. The management aims to grow this segment at the industry rate of 20 per cent in the current financial year and is also planning to sell 26 per cent stake to a strategic investor.

After a slight uptick in the gross non-performing assets (NPAs) of its NBFC to 1.9 per cent in the December 2012 quarter, the management expects this metric to improve to 1.7 per cent due to recoveries picking up. Going forward, it aims to improve return ratios as well.

Says Sam Ghosh, chief executive officer, Reliance Capital, “We plan to improve our margins and expect the return on equity ratio in the lending business to improve from current levels of 12 per cent to about 18 per cent. We expect to grow the loan book by 5-10 per cent this financial year.” Peers like L&T Finance and M&M Financial are expected to grow their FY13 loan book by 15-30 per cent.