"The Mark Mobius pick that bombed")

Soon after the deal, Mobius, executive chairman of TAML, said: “We are impressed with Shiv-Vani’s oil and gas exploration services capabilities and are confident these can be leveraged to assist oil & gas companies around the world.” The investment, he was confident, would fund the ongoing equipment and technology needs to make Shiv-Vani a force to reckon with in the global arena for exploration services. “This investment fits well with our global exposure to the energy sector and we look forward to working with Shiv-Vani’s management and promoters to make this a landmark relationship,” the star fund manager had said.

Strengthening this outlook, Rohan Consultancy Services, a promoter group entity, purchased 277,178 shares in May 2010 at Rs 423 a share.

As Mobius had said, Shiv-Vani was ideally positioned as the largest onshore rig owner-cum-operator to benefit from the Union government’s expansion plans and increased spending in onshore exploration. It also had a healthy order book of around Rs 4,000 crore, in a sector where entry barriers are high. Most important, Shiv-Vani had a healthy business relationship with the government’s Oil and Natural Gas Corporation (ONGC), the largest exploration entity. It certainly looked like a good investment.

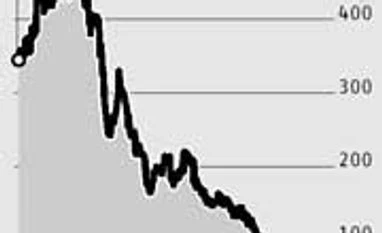

Today, Shiv-Vani shares are trading around Rs 28 and show no sign of recovering. At this price, the entire company is valued at a paltry Rs 130 crore. At current exchange rates, this is marginally above $20.6 million, the amount Templeton paid for its 5.3 per cent stake three years earlier.

In it, along with Templeton, are other marquee names such as Citi Venture, Reliance Capital, Aviva Life and Religare Finvest. Is this 93 per cent crash in stock prices justified or are the prices running ahead of fundamentals?

Templeton, which has since raised its stake to eight per cent, did not respond to an email query on the investment. A Templeton India spokesperson said the fund did not comment on stock-specific queries.

What went wrong?

Fund managers with exposure to the company said Shiv-Vani has been facing trouble on multiple fronts over several months and has not done enough to fight these. While the business outlook became grim following lower government spending, several operational issues erupted as the company found it difficult to service high-cost debt. Investor circles also said the company had initially benefited from association with the brass in some public sector firms, whose contracts it was executing, and suffered when these ties snapped.

Gupta dismissed the conspiracy theories but agrees things got difficult when ONGC, Shiv-Vani’s primary client, was in the middle of a leadership change. “ONGC was headless for about a year. Contract renewals did not take place during the period. This affected the cash flow.” These financial constraints made the company default on tax payments.

In January this year, the Central Board of Excise and Customs registered a case of service tax evasion of Rs 200 crore. Reports said the firm had not filed service tax returns since October 2010. The company agreed to the liability but cited “financial constraints” for non-payment.

What could be the financial constraints of a company that made revenue of Rs 1,484 crore in FY12 and net profit of around Rs 200 crore every year since FY09?

Suspicion

Some lenders fear the worst. “Based on our diligence, we believe the company is inflating its (annual) revenue by $80-90 mn. Accordingly, the number of rigs could be inflated by 30-40 per cent, assuming a few are genuinely idle,” said a creditor in an internal note reviewed by Business Standard. The note says of the 40 rigs claimed to have been owned by the company, only 15 were credibly verifiable. A fund manager with an exposure to the hybrid instruments of the company also said, “The company claims it has deployed 12 rigs with ONGC. Our own diligence showed they had only six.”

By the company’s latest financials, the gross block was around Rs 3,000 crore. “According to our estimates, Shiv-Vani probably spent around Rs 1,200 crore acquiring equipment,” the note added.

Gupta said he’d already adequately addressed several queries raised by the creditors. “Of the 40 rigs, 17 were 1,000 Hp or more. This is the minimum capacity required in drilling.” According to him, three of the remaining rigs were deployed in Oman. “Of the smaller rigs, we have got regular contracts running on five more, though these account for very little revenue. Other rigs are idle.”

The company has been blacklisted by some private sector exploration companies, such as Cairn India. Recently, Oil India, another state-owned explorer, sought vigilance department clearance for contracting the services of Shiv-Vani, though it was the lowest bidder.

It was also briefly banned by ONGC for certain violations. Gupta brushed it aside as a minor issue. “There was a small contract on compression services. We should not have applied for that. But, we wanted to use machinery which was lying idle. Instead of deploying staff, we had outsourced it. This person could not complete the job due to some issues. We explained the situation and ONGC accepted it. This matter has been blown out of proportion.”

Now

On the falling stock prices, Gupta said investors in India are yet to understand the nature of this business. “I don’t have much control over stock prices. Globally, this business is highly geared. Here people look at the debt-equity ratio, refer to the FCCB (foreign currency convertible bond) liabilities and get worried.” The company has raised FCCBs worth $80 mn, maturing in August 2015. Several public and private sector lenders have also lent to Shiv-Vani for purchase of equipment and other capital expenditure. These include ICICI Bank, State Bank of India, Punjab National Bank, YES Bank, Corporation Bank and IFCI.

A total of 57 promoter group entities, led by brothers Prem and Padam Singhee, own 49.38 per cent in the company. As the debts mount, about 85 per cent of these shares held by the promoter group are pledged with lenders. This could also be putting pressure on the stock prices, as every fall triggers new margin calls and fresh selling creating a vicious cycle, say analysts.

Even as some lenders began asking tough questions, Shiv-Vani moved for a corporate debt restructuring (CDR) plan. Gupta hopes the company will bounce back after the CDR. “The restructuring of debts will result in improvement in the liquidity and strengthen the core operations, which will lead to value addition of the stake holders in the long term.”