"Three stocks that could defy the IT slowdown")

At a time when the larger software services firms are facing multiple headwinds, thanks to digitisation as well as rising protectionism, niche information technology (IT) companies offering engineering research and development (ER&D) services are in a sweet spot.

Indian IT companies have grown at a rapid pace of 15 per cent in the ER&D space over the last five years and this segment is largely unaffected by the disruption caused by digitisation.

“Mid-cap companies focused on specialising either on the digital side or in product engineering are more of a partner to their clients and are better placed than larger companies,” said Parag Gupta, IT analyst at Morgan Stanley.

Among the large-cap companies, HCL Technologies derives the largest proportion (19 per cent) of revenues from the ER&D space and is among the top ER&D outsourcing companies globally.

“Lower penetration of ER&D services, increasing outsourcing to Indian companies and lower exposure to the current disruptive trends being witnessed in IT services are positives for these companies,” said Rakesh Tarway, head of research at Reliance Securities.

Cyient and HCL Technologies are his top picks. ER&D is the third largest service provided by HCL Technologies, which with application services and infrastructure services, contribute 77 per cent to total revenue.

Against this backdrop, investors can consider mid-cap companies having a greater exposure to the high-potential ER&D segment.

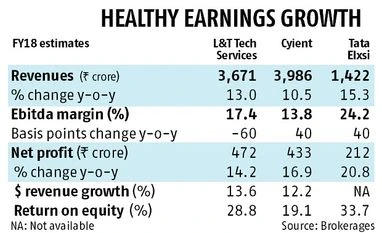

L&T Technology Services derives 100 per cent of its revenue from ER&D and works with 44 of the top 100 ER&D spending companies. Strong parentage under the L&T umbrella has propelled the company to leadership position in the industrial products segment with access to marquee clients (Unilever, P&G, Shell). Its management is confident of delivering double-digit growth in 2017-18.

Given that it is the only pure-play listed ER&D company, analysts believe it should trade at premium valuations to peers like Cyient. The stock trades much below its IPO price of Rs 860 at 15 times 2017-18 estimated earnings and could witness 15-20 per cent upside from current levels, analysts said.

Cyient, earlier known as Infotech Enterprises, derives 62 per cent of its revenue from ER&D. It is witnessing healthy traction across aerospace and defence, communications, rail transportation as well as from its top clients. Its relatively lower exposure to visa-based workers in the US protects it against stringent norms on this front.

Unlike its larger peers, inorganic expansion forms a vital part of Cyient’s growth and the company has a successful track record here. Increasing utilisation and higher offshoring could drive a 100-120 basis point improvement in its operating profit margin in the next two years, analysts said.

Tata Elxsi has a relatively higher focus on the engineering design segment. Jaguar Land Rover (JLR) is a client providing 22 per cent of revenue alongside other marquee global automobile makers. Broadcast and communications are other key segments the company operates in. A rising presence in Japan apart from strong momentum in the US and Europe and a stronger focus on finding attractive inorganic avenues could drive future growth.

The company’s efforts to adapt a revenue sharing model linked to efforts as well as success could boost margins by as much as 100-200 basis points over the next two-three years, according to Chintan Modi, analyst at Motilal Oswal Securities.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in