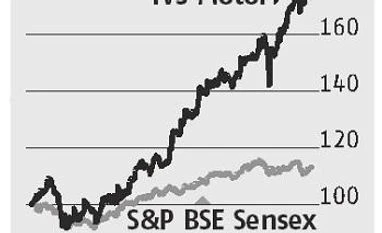

"TVS Motor in the fast lane")

The TVS Motor stock has been hitting successive 52-week highs on strong volume performance in September and market share gains in the two-wheeler space. The company is also expected to post strong September quarter (Q2) results.

TVS Motor’s volumes in September were up 23 per cent year-on-year (yoy), led by a 43 per cent rise in scooter despatches. Scooters account for 34 per cent of the company’s volumes.

The increased preference for scooters is expected to help the company gain on the volumes and market share fronts.

The share of scooters in the two-wheeler industry’s volumes increased 400 basis points (bps) yoy to 34 per cent in the June quarter (Q1), led by demand in the southern region. Scooters now account for 45 per cent of two-wheeler sales in this region.

TVS Motor’s market share in the scooter segment increased 50 bps y-o-y to 13.8 per cent in the June quarter. Its scooter portfolio includes the Wego, the Jupiter, the Scooty pep+ and the Zest.

Exports and strong sales of motorcycles and three-wheelers are also helping the firm.

While sales of three-wheelers were up 54 per cent, motorcycles’ volumes rose 17 per cent and exports grew 33 per cent in September over the year-ago period.

After reporting single-digit growth in Q1, the sector’s double-digit growth in Q2 has led analysts to revise upwards their volume estimates for the company and the industry.

A rebound in two-wheeler sales has helped the company report a 16 per cent gain in volumes in Q2. Analysts at Kotak Institutional Equities said the company was one of the three automakers (the others being Ashok Leyland and Eicher Motors) which were expected to outperform in the September quarter.

Revenue growth for the company could come in at 20 per cent yoy, given better sales mix, while improvement in average selling prices are led by the higher-margin spare parts and three-wheeler segments. Even more than volume and revenue gains, the Street will be watching out for TVS Motor’s margin trajectory.

According to analysts, margins in Q1 at 6.2 per cent were impacted by the goods and services tax-related dealer compensation and higher discounts to clear inventory.

The volume uptick, coupled with an improved product mix and higher sales of established brands such as the Apache and the Jupiter, should help to improve the margins.

Analysts at Sharekhan expect the company to report operating profit margins of 8.3 per cent and 9.8 per cent in FY18 and FY19, respectively.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in