"Under bond market pressure, PSBs stare at Rs 75-90 bn MTM loss this quarter")

Already weighed down by a pile-up of bad loans, bond market pressure is making the situation worse for public sector banks (PSBs). These institutions are the biggest investors in government bonds (G-secs).

Under Reserve Bank of India (RBI) guidelines, banks need to allocate a portion of their operating profit to offset any mark-to-market losses (notional losses from revaluing of assets at current prices) due to erosion of bond value under the Available for Sale (AFS) category.

Some PSBs lowered their AFS portion in the June quarter but still have a sizable amount. As of June end, the AFS book of the top five PSBs accounted for 21-47 per cent of their respective investment pie.

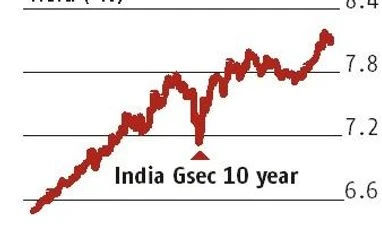

Bond prices are inversely related to yields, the latter currently around 8.1 per cent (up 20 basis points up since June).

RBI’s open market operation (OMO) on Wednesday to purchase Rs 100 billion in G-secs is unlikely to move the needle by much. “The system is already in deficit liquidity. So, OMO would help restore equilibrium in liquidity but might not help to bring down yields,” says Madan Sabnavis, chief economist at CARE Ratings.

“At the end of September, yields would remain at 8.15-8.2 per cent and above eight per cent through the rest of FY19.”

This means PSBs would have to provide for MTM losses even for a third consecutive for September 2018 quarter (Q2), further denting their capital. In the June quarter, MTM provisioning accounted for 16-60 per cent of many PSBs’ pre-provisioning operating profit.

Notably, some banks had exercised the RBI-given option of spreading MTM losses equally over four quarters.

If G-sec yields stand at 8.2 per cent at the end of the September quarter, PSBs would have to provide Rs 75-90 billion for MTM loss or 20-24 per cent of the combined operating profit in the June quarter.

“As per our calculation, for every 10 basis point (bp) rise in yields, PSBs have to bear Rs 30 billion in MTM loss,” says Anil Gupta, head of financial sector ratings at ICRA. Other analysts peg MTM losses at Rs 25 billion for a 10 bp rise in yield.

Also, some PSBs will need to take care of their carried-forward MTM loss. The RBI had, as mentioned earlier, allowed banks to spread MTM losses since the December 2017 quarter equally over four quarters. Some banks had done so.

According to ICRA, such carried-forward MTM burden of PSBs stands at around Rs 85 billion as of June end. ICRA estimates this carried-forward MTM burden of PSBs at Rs 85 billion as of June end.

Even going ahead, bond market pressure is unlikely to soften. “The market is currently anticipating a 25-bps rate hike by RBI. Yields could be even higher if the rate hike is 50 bps during the rest of the year,” Sabnavis added. There are more chances of the latter choice by RBI amid macro headwinds such as a weak rupee and high crude oil prices. Further, the second half of FY19 will witness more government spending, putting further pressure on bond yields.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in