"Value-added segment to help copper smelters offset margin pressure")

A sharp decline in income from the copper business due to lower treatment and refining charges (Tc/Rc) is a concern for India’s primary base metals producers including Hindalco Industries and Vedanta, but their focus on value-added copper products and firm aluminium prices should help offset any potential income decline in the copper business.

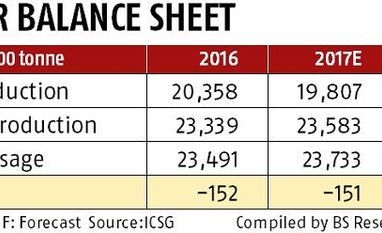

Global copper smelters led by Jiangxi Copper Corporation and Guixi of China are negotiating with global miners for conversion charges ranging at $70-89 a tonne (Tc) and refining charges (Rc) of US cents 7.0-8.9 a pound (about 450 gm) for the calendar year (CY) 2018. These ranges of Tc/Rc works out to 3-24 per cent lower than $92 a tonne (Tc) and US cents 9.2 (Rc) global smelters realised in CY2017.

India’s custom copper smelters including Hindalco and Vedanta procure concentrate from global miners on both long-term contract as well as on a spot basis and earn Tc/Rc from their business. Variations in Tc/Rc determine an increase or decline in the top line and bottom line of their copper smelter business. Currently, global smelters see $80-85 a tonne of Tc and US cents 8.5 a pound as Rc as profitable. Almost a similar profit benchmark works out for Indian smelters including Hindalco and Vedanta.

“Global smelters are yet to arrive at a final decision on Tc/Rc. Over the last few years, we have worked out hard to reduce our cost of copper production through improvement in plant efficiency and diversification towards value-added products so that we would be able to make up for the (any) decline in Tc/Rc. Our new copper rods plant is expected to start commercial production sometime in April next year. Despite that, reduction in Tc/Rc will certainly have an impact on margins of our business,” said P Ramnath, chief executive officer, Sterlite Industries (India), the copper division of Vedanta.

Hindalco and Sterlite Industries have an installed copper production capacity of 500,000 tonnes and 400,000 tonnes, respectively.

Their respective capacity utilisations stood at 75.4 per cent and 100 per cent for FY17. Both Hindalco and Vedanta posted an increase in their earnings from the copper business in the September quarter despite lower volumes due to a sharp increase in their realisation from the currency and commodity businesses.

“Globally, the Tc/Rc rates for copper are likely to weaken in the near term on account of constrained mine supplies, which is likely to have an adverse impact on the profitability of custom smelters. In India, while the copper businesses of large players like Hindalco and Vedanta would be impacted, the same is likely to be offset by an expected margin improvement in the aluminium business in the case of Hindalco. However, the same for Vedanta will be partially negated by rising costs of aluminia and carbon, since it has to depend upon external sources of bauxite/alumina,” said Jayanta Roy, senior vice-president (Group Head - Corporate Sector Ratings), ICRA.

Outside the base metals business, Vedanta, however, could also find some cushion from rising oil prices, given its exposure through Cairn India, which produces close to 200,000 barrels of oil per day in its Rajasthan-based hydrocarbon assets. A small support could also come from firm iron ore prices.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in