"5 high-yield stocks worth picking")

The last five years, from 2008, have been the most difficult for India Inc in terms of growth and managing of finances. With growth rates decelerating sharply, both in India and globally, and liquidity not easily available, many companies have been impacted. This is also reflected in share prices; a large number of stocks and indices have moved nowhere in all these years, disappointing investors. In fact, many stocks are currently trading below the levels seen in 2008.

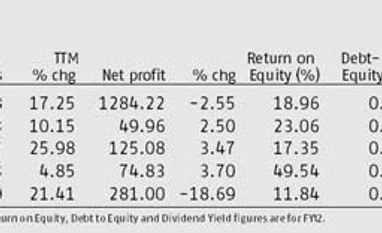

In this difficult period, if a company has consistently reported profits, maintained dividends, generated positive cash flow from operations and earned healthy return on equity (RoE), it demands special mention. Here are five such companies, which not only meet these criteria and offer high dividend yield but also have less debt in the books and, importantly, are also likely to do well in the longer run.

IL&FS Investment Managers

An IL&FS group company, this operates in the private equity space and runs several thematic funds in infrastructure and real estate, among others. It has grown consistently. From Rs 60 crore in FY07, turnover has risen to Rs 220 crore in FY12. In this period, after doubling to Rs 62 crore in FY09, annual profits have been Rs 70-75 crore, aided by an asset-light business and lower costs of operations. This allows it to maintain dividends, due to internal cash generation. In the past three to four quarters, it has been able to grow its revenue and profits, albeit in single digits, which should improve once the economy looks up. At current levels, while valuations are reasonable, the stock is also offering a high dividend yield of 7.1 per cent.

NRB Bearings

While India’s top ball bearings makers are facing tough times, given the slowing in the automobile segment, NRB Bearings has been ahead of its peer group in terms of sales and net profit growth over the past three years. Given the slowdown in the domestic auto space, higher exports have boosted its revenues in recent quarters. Although FY12 saw a marginal dip in consolidated profits, mainly due to doubling of interest outgo to Rs 15 crore and a rise in depreciation, the nine months of FY13 saw an improvement in both top line and bottom line (five to eight per cent).

The increase in share of revenues from the replacement market, as well as exports (15 per cent each, currently), and uptick in the economic cycle is likely to aid revenue growth. Given the stock correction (down 25 per cent over six months), it is trading at less than five times its FY14 estimates, with decent cash flows and high dividend yield providing support.

Andhra Bank

Public sector banks have remained in the news over issues of growth and non-performing assets. Though business growth is expected to remain moderate in the next few quarters, the comforting factor is that the asset quality is stabilising and margins are expected to improve. Within this space, Andhra Bank, which has fallen 26 per cent in a year, is currently offering a dividend yield of six per cent. This is good for a bank with 16 per cent RoE and trading at 0.6 times its estimated book value in FY13. The decline in its trailing 12-months profits can be attributed to the additional provision of Rs 44 crore it had to make in line with new regulations in the December 2012 quarter. Earnings growth over the next two years is estimated at 16-18 per cent.

Gateway Distriparks

The slight uptick in container volumes over the past two months, recent reduction in haulage charges, market share gains and expanding network make Gateway Distriparks a preferred pick (in the logistics segment) among analysts. What tilts the scales in favour of the company — operating in the container storage, rail transport and cold chain segments — are the valuations, with its FY14 earnings multiple at around eight times and the price to book at 1.5 times. The dividend yield at around of five per cent adds to the stock’s attractiveness.

Given the decent returns ratios (14-16 per cent), operating profit margins (25 per cent) and business prospects, expect the cash flows to be strong. Given the nature of the business, the negligible debt on the books is positive and will allow the company to invest for growth as the economic situation improves.

GNFC

GNFC is among India’s leading fertiliser and industrial chemical companies and scores well on consistency. High core RoE, robust internal cash flows and low leverage makes it a preferred pick in this category. The stock valuation of just three times its FY14 estimated earnings is attractive, given the company’s expected growth and strong position in an industry which is less cyclical.

GNFC has been expanding its capacity and has invested about Rs 400 crore in two years. The benefit of this will start reflecting from FY14 onwards. The revenue growth over the next two years is expected to be in the region of 15-20 per cent annually, which should result in strong earnings growth.

In this difficult period, if a company has consistently reported profits, maintained dividends, generated positive cash flow from operations and earned healthy return on equity (RoE), it demands special mention. Here are five such companies, which not only meet these criteria and offer high dividend yield but also have less debt in the books and, importantly, are also likely to do well in the longer run.

IL&FS Investment Managers

An IL&FS group company, this operates in the private equity space and runs several thematic funds in infrastructure and real estate, among others. It has grown consistently. From Rs 60 crore in FY07, turnover has risen to Rs 220 crore in FY12. In this period, after doubling to Rs 62 crore in FY09, annual profits have been Rs 70-75 crore, aided by an asset-light business and lower costs of operations. This allows it to maintain dividends, due to internal cash generation. In the past three to four quarters, it has been able to grow its revenue and profits, albeit in single digits, which should improve once the economy looks up. At current levels, while valuations are reasonable, the stock is also offering a high dividend yield of 7.1 per cent.

NRB Bearings

While India’s top ball bearings makers are facing tough times, given the slowing in the automobile segment, NRB Bearings has been ahead of its peer group in terms of sales and net profit growth over the past three years. Given the slowdown in the domestic auto space, higher exports have boosted its revenues in recent quarters. Although FY12 saw a marginal dip in consolidated profits, mainly due to doubling of interest outgo to Rs 15 crore and a rise in depreciation, the nine months of FY13 saw an improvement in both top line and bottom line (five to eight per cent).

The increase in share of revenues from the replacement market, as well as exports (15 per cent each, currently), and uptick in the economic cycle is likely to aid revenue growth. Given the stock correction (down 25 per cent over six months), it is trading at less than five times its FY14 estimates, with decent cash flows and high dividend yield providing support.

Andhra Bank

Public sector banks have remained in the news over issues of growth and non-performing assets. Though business growth is expected to remain moderate in the next few quarters, the comforting factor is that the asset quality is stabilising and margins are expected to improve. Within this space, Andhra Bank, which has fallen 26 per cent in a year, is currently offering a dividend yield of six per cent. This is good for a bank with 16 per cent RoE and trading at 0.6 times its estimated book value in FY13. The decline in its trailing 12-months profits can be attributed to the additional provision of Rs 44 crore it had to make in line with new regulations in the December 2012 quarter. Earnings growth over the next two years is estimated at 16-18 per cent.

Gateway Distriparks

The slight uptick in container volumes over the past two months, recent reduction in haulage charges, market share gains and expanding network make Gateway Distriparks a preferred pick (in the logistics segment) among analysts. What tilts the scales in favour of the company — operating in the container storage, rail transport and cold chain segments — are the valuations, with its FY14 earnings multiple at around eight times and the price to book at 1.5 times. The dividend yield at around of five per cent adds to the stock’s attractiveness.

Given the decent returns ratios (14-16 per cent), operating profit margins (25 per cent) and business prospects, expect the cash flows to be strong. Given the nature of the business, the negligible debt on the books is positive and will allow the company to invest for growth as the economic situation improves.

GNFC

GNFC is among India’s leading fertiliser and industrial chemical companies and scores well on consistency. High core RoE, robust internal cash flows and low leverage makes it a preferred pick in this category. The stock valuation of just three times its FY14 estimated earnings is attractive, given the company’s expected growth and strong position in an industry which is less cyclical.

GNFC has been expanding its capacity and has invested about Rs 400 crore in two years. The benefit of this will start reflecting from FY14 onwards. The revenue growth over the next two years is expected to be in the region of 15-20 per cent annually, which should result in strong earnings growth.