"Why optimism should be tempered")

Even as BSE’s initial public offering of shares breaks records and brings cheer, a critical question remains: How long will the party last? No clear answers, but ordinary financials of exchange firms listed abroad put sustainability in doubt.

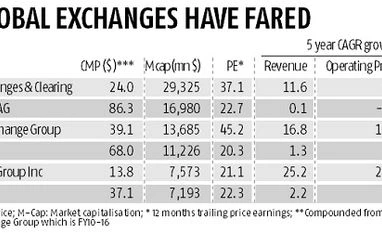

Today, the parent company of one of the oldest stock exchanges in the world faces merger with London Stock Exchange Group. Frankfurt Stock Exchange's Deutsche Börse AG has seen its net profits dwindle year after year since 2010; revenue growth has been flat. Three years ago, London Stock Exchange Group was weak, too, until aggressive product launching and tech push - steps needed to combat lacklustre trade volumes - kicked in. But Nasdaq Inc, which owns the Nasdaq exchange in the United States, hasn't seen the same success with new products. Its revenues have grown just over one per cent since 2010, while net profit, if not for investment income, would have grown lower than seven per cent over this period. Hong Kong Stock Exchange and Clearing Limited, which owns the Hang Seng Index of China, has at least performed better than its peers in the West. While its revenues over FY10-15 have increased 12 per cent, its net profit has increased only 8.6 per cent in this period. As a result, its market capitalisation grew only eight per cent in the past five years, indicating not much reward for investors.

All the cheers for the listing of India's BSE (formerly Bombay Stock Exchange) and National Stock Exchange (NSE) need review against this backdrop. Trade volumes don't show healthy growth for both. And BSE's less than three per cent CAGR (compound annual growth rate) in revenue over FY12-16, as well as 6.7 per cent decline in net profit over the period, don't come as a surprise either. NSE, too, hasn't been great, with revenues increasing just 5.6 per cent CAGR and net profit growing 1.8 per cent over this period. Both these exchange companies have largely benefitted from revenues of their depository businesses: Central Depository Services Limited, owned by BSE, and National Securities Depository Limited of NSE. Central Depository Services Limited is gearing up for public issuance, which may reduce investment income support for BSE. National Stock Exchange runs the same risk. Investment incomes, after all, can help the exchange company meet operating expenses and even make up for declining income from core operations. Business from mainstay (trading and listing of shares) has grown only two per cent at BSE and six per cent at NSE since FY12. While both celebrate newer streams of revenue such as data solutions, mutual fund distribution, and corporate services, the core business shows weakness. Nonetheless, home-bred status and overall positive sentiment may assure good listing gains for BSE and NSE, but looking at past and peer performances, sustainability of these gains will remain in question.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in