Can spurt in crude oil prices trigger rally in commodities?

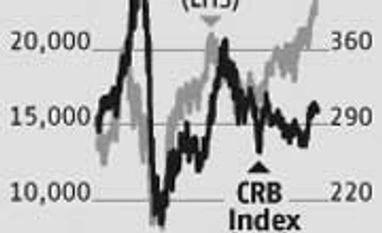

CRB commodity index is showing bullish buoyancy and trading above its 200-day moving average

Krishna Kant Mumbai Is the market at the cusp of a rally in commodities? Crude oil prices have soared on news of turmoil in Iraq, one of the world's top oil exporters. West Texas Intermediate Crude, the US benchmark, gained over 2 per cent and hit an eight-month high. This rattled equity markets and the Sensex tanked nearly 350 points on Friday.

The market reaction to higher crude oil prices is not surprising. India is one of the world's top crude oil importers and higher crude oil prices would translate into higher consumer inflation, losses for government-owned oil refiners and increased fuel subsidy and higher fiscal deficit. This is a recipe for poor GDP growth and market volatility.

Equity investors, however, should brace for more bad news on crude oil and commodity prices. The same factors that support a rally in equities also support higher crude oil and commodity prices, at least in the short term.

The world's top central banks continue to follow an easy monetary policy and low interest rate regime in a bid to perk economic growth and employment in the developed world. This has resulted in the Libor rate falling to a 30-year low in the London inter-bank lending market. The interest rate on the 12-month US dollar Libor is down to 0.54 per cent, against 0.68 per cent a year ago and average of around 1.6 per cent in 2009.

Given the anaemic economic growth and poor state of corporate investments in the world's top economies, it is natural for the gush of liquidity to finds its way into various asset markets. In 2012, capital flew into high-yielding equity markets in emerging markets while 2013 saw a record rally in Japanese equity markets and other developed markets. Investors have booked profits in Japan this year and are back in emerging markets, leading to a rally on Dalal Street. But there is a limit to the amount of capital that markets like India can absorb in the absence of a quick recovery in corporate earnings.

So far, investors had the luxury of ignoring the commodity front, given the lack of price triggers. Recent political disturbances in key oil producing countries such as Russia, Libya, Syria and Iraq could be the starting point.

The Thomson Reuters CRB commodity index which tracks prices of 19 commonly traded commodities, including crude, metals, gold & silver and agriculture commodities, has been range-bound for over two years even as equity markets have made new highs globally. The index is now showing buoyancy and is firmly trading above its 200-day moving average, a bullish signal (see chart).

In the past, commodities and equities have moved in tandem albeit with a lag. For the first time in the last seven years, the CRB Index and the S&P BSE Sensex have moved in opposite directions. This happy coincidence is not likely to last long, given the inter-connected nature of various asset markets and a common set of investors chasing yields across the globe.

"Can spurt in crude oil prices trigger rally in commodities?")