"Chaos may cast a shadow on global trade")

The last fortnight has been marked by an escalation in geopolitical tensions and there's every likelihood that the tensions will remain high. On the domestic front, the shock resignation of Reserve Bank of India (RBI) Governor, Urjit Patel, will have a negative impact on market sentiment, which was already low due to the prospect of the BJP losing ground in assembly elections.

Abroad, after Russia “confiscated” Ukrainian naval vessels, there were riots in France, big anti-Brexit demonstrations in the UK, and Angela Merkel appointed her political successor. The CFO of Huawei, who is also the daughter of the founder, was arrested in Canada at the behest of US authorities. That caused outrage in Beijing and derailed talks on a possible resolution of the Trade War. Special Counsel Robert Mueller’s indictments of two key Trump aides brings the probe into campaign violations into closer proximity to the White House. Apart from sentiment, there could be economic consequences as these events will be unfavourable for growth.

The Organisation of the Petroleum Exporting Countries (Opec) meeting in Vienna led to an agreement that the oil cartel and Russia will cut production by 1.2 million barrels a day. That led to a spike in crude prices and created renewed pressure on the rupee.

This may influence the Federal Reserve into pausing its schedule of rate hikes. Across the Atlantic, the European Central Bank may also decide to avoid tapering its ongoing Quantitative Easing Programme, if it decides it needs to counter a possible EU slowdown.

Those key central bank reviews will influence market direction. If the Fed does hike anyway, alongside its ongoing quantitative tightening programme and the ECB decides to taper anyhow, there would be a loss of hard currency money supply. That would certainly affect all markets.

The factors behind Patel’s resignation are not known. Rumours apart, it is bound to have a negative effect since it leaves the central bank headless at a crucial moment. There was no hint of this last week, when the Monetary Policy Committee decided to stand pat on policy rates. There was a case for a rate cut, due to lower inflation and slower GDP growth. The RBI is also holding to earlier growth projections, while it has cut its inflation projections. The review hinted that the MPC could hold rates again in February. But it issued a warning about the necessity for fiscal discipline.

The fiscal deficit has already crossed the full year budget estimates and expenditure is unlikely to be cut given electoral compulsions. The current account deficit is running at 2.9 per cent of GDP but it may reduce if crude prices stay down.

GST collections for December-March would need to rise by about 45 per cent above current levels to meet Budget estimates. That sort of tax surge seems unlikely, given a Q2 slowdown and poor signals from the auto market. Auto sales in November, during festivals, were dismal. Dealers say that they are holding high inventory and rural demand has dropped, due to agrarian distress. Honda was the only auto-major that saw higher unit sales during the Diwali season. Commercial vehicle sales also slipped into the red as did two-wheeler sales. Higher insurance rates and high EMIs were cited as dampeners, along with expensive fuel.

The government is going through the usual cross-holdings method of raiding PSU reserves to try and meet disinvestment targets. The PFC-REC deal follows the same pattern as the ONGC-HPCL takeover last year. The government retains control, nothing changes, except for a transfer of reserves from a corporate entity to the consolidated fund. As with ONGC-HPCL, any borrowings PFC undertakes will impact the PSU’s balance sheet. It is a terrible way to treat minority shareholders but it is also a time honoured tradition. Assuming aboutRs140 billion comes in on this front, this will push disinvestments close to aboutRs460 billion for the fiscal, The target isRs800 billion. So, we might see more such deals.

In other developments on the corporate front, the Sun Pharma investigation could lead to new cans of worms being opened. More details also continue to emerge about the state of IL&FS’ finances, suggesting it is an even larger mess than was earlier apparent.

The Unilever-GSK Consumer deal has hit what could be a temporary roadblock. Steer Engineering wants assurances that its Intellectual Property will be protected and the Delhi High Court will hold its next hearing about this issue on January 23.

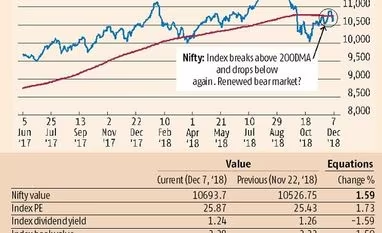

Sentiment is down therefore, and likely to stay down, until the geopolitical tensions cool off and there is some clarity on the RBI successor, and domestic political issues. Both domestic institutions and FPIs have sold heavily in the past ten sessions. Technically, the Nifty made a failed breakout, moving above the 200 Day Moving Average, and then correcting back below again.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in