"Companies rejig joint ventures to meet IndAS norms")

The adoption of the new Indian Accounting Standards (IndAS) might bring about a sea change in the way joint ventures and many private equity investments are structured in corporate India.

Typically, joint ventures (JVs) are governed by an agreement between the parties laying down the purpose of the venture, each party’s contribution, control and share of profit.

Companies are now closely evaluating these agreements to determine whether they have unilateral control over the important decisions involving the JV — including appointment of board of directors, approval of operating budgets, and appointment and remuneration of key personnel.

This is especially the case with companies in sectors such as real estate, infrastructure, power generation, aerospace and defence, and oil and gas where JV arrangements are common. Arrangements could be between domestic partners, or between domestic and international partners. It could be strategic ventures with one party holding, say, 51 per cent stake and the other 49 per cent, or financing arrangements where private equity players hold much smaller stakes. “In many of these negotiations, the ability to consolidate the operations of the entity has become one of the most critical issues for discussion between parties as they seek to enter into strategic partnerships with other companies or financing arrangements with PE firms,” said Sai Venkateshwaran, partner & head-accounting advisory services, KPMG India. Consolidation here implies to consolidation of the balance sheet and the profit and loss statement of the JV entity with the parent company.

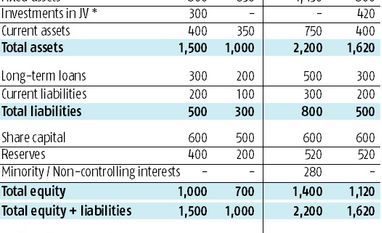

Several Indian companies had previously entered into joint venture arrangements where they could do a full consolidation of the company as long as they held more than 50 per cent, even though the other partners may have had joint control on the entity. This was due to a specific provision in the older accounting standards that permitted companies to be consolidated based on the majority ownership interest. Further, the two parties could consolidate the same JV company using either different frameworks (one under Indian GAAP and other under IFRS) or using different aspects of the definition of control (one based on majority share ownership and the other based on the power to appoint majority members on the board, etc).

However, the assessment is different under IndAS, and is based more on the substance of an arrangement of how the entity is controlled and managed. Additionally, these standards also recognise that there can’t be more than one party controlling an entity.

“Due to the IndAS requirements, many entities that were previously consolidated, either in full or on a proportionate basis, under the older Indian GAAP, will now need to be deconsolidated and accounted under the equity method, thereby shrinking the size of the balance sheet and P&L for many companies,” added Venkateshwaran.

Under IndAS, none of the parties to the joint ventures would be able to do full consolidation, but would only be able to do equity accounting. This method involves a single line consolidation for share of profits/losses of the JV. Under the full consolidation method, the parent’s and subsidiary’s operations are presented on a single set of consolidated financial statements. Under the equity method, the parent's financial statements include a line for investment in an associate or joint venture that is equal to the owned share of the subsidiary's net assets/equity.

To this end, companies are evaluating legal agreements involving their investments in other entities. The critical aspect being looked at is the ability to consolidate the operations of the JV entity and whether a partner has unilateral control over the relevant and important decisions of the JV company, which is the determining factor for being deemed a controlling entity.

The decisions that are being closely evaluated could include acquiring or disposing of assets, determining a funding structure or obtaining funding, establishing operating and capital decisions of the investee, including budgets and appointing and remunerating the other entity’s key management personnel.

“An entity could control another with even less than majority ownership of equity or voting interest, so long as the contractual or shareholder arrangements allow the entity to direct the important and relevant activities. Additionally, even if an entity’s existing equity ownership is less than 50 per cent in a JV, one will have to take into account potential voting rights such as warrants and call options to evaluate control,” added Seth.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in