"Crowding out and opening up")

Finance Minister Nirmala Sitharaman prepared the Union Budget for 2020-21 while labouring under multiple constraints. The economy has slowed sharply. Tax revenue is lower than expected by perhaps 0.7 per cent of gross domestic product or GDP — though what proportion of this is due to the economic slowdown and what to problems with goods and services tax (GST) cannot easily be determined. Political constraints continue to operate on the Budget process, given that this government is in perpetual election fighting mode, and the prime minister’s office is known to be exceptionally active. While Ms Sitharaman has demonstrated that she has little time for interest groups demanding special or sectoral benefits, it is also true that even experts are divided on what is the best response at this time — to ignore fiscal constraints in order to stimulate demand for the short run, or to continue to exercise restraint while pushing forward structural reform using this moment of crisis.

In the end, the FM appears to have chosen, as most in her position before her have, to attempt to find a via media between these two approaches. The fiscal glide path was altered — on paper — only as much as the Fiscal Responsibility and Budget Management Act allows, while spending was controlled, but not to the degree that might be warranted, given the crunch in revenue. In some sense, any such Budget will be seen by both sides of the debate as a “disappointment”.

Certainly, the equity markets, which were open and trading on Budget Day although it was a Saturday, seem to have reflected such a disappointment. Some must have hoped that a big fiscal stimulus was in the works that would have “revived” consumer demand and perhaps spilled over into corporate earnings. I am uncertain, however, about the thought processes that underlay this expectation. After all, many people also believe that tax evasion has been widespread under the new GST system. If GST is underperforming by as much as a percentage point of GDP thanks to evasion, what does that mean? Certainly, if the tax to GDP ratio has declined since 2017-18, partly due to indirect taxes remaining in the hands of the population, does that not count as a stimulus of equivalent size?

In the end, the FM appears to have chosen, as most in her position before her have, to attempt to find a via media between these two approaches. The fiscal glide path was altered — on paper — only as much as the Fiscal Responsibility and Budget Management Act allows, while spending was controlled, but not to the degree that might be warranted, given the crunch in revenue. In some sense, any such Budget will be seen by both sides of the debate as a “disappointment”.

Certainly, the equity markets, which were open and trading on Budget Day although it was a Saturday, seem to have reflected such a disappointment. Some must have hoped that a big fiscal stimulus was in the works that would have “revived” consumer demand and perhaps spilled over into corporate earnings. I am uncertain, however, about the thought processes that underlay this expectation. After all, many people also believe that tax evasion has been widespread under the new GST system. If GST is underperforming by as much as a percentage point of GDP thanks to evasion, what does that mean? Certainly, if the tax to GDP ratio has declined since 2017-18, partly due to indirect taxes remaining in the hands of the population, does that not count as a stimulus of equivalent size?

There are legitimate questions that might be asked whether the fiscal deficit has indeed been contained and will be contained to the headline levels. The FM has been far more transparent than has been the practice in recent years, by making some extra-Budgetary borrowing explicit, and showing how much that pushes up the actual fiscal deficit. However, the fact remains that some other borrowing by quasi-government agencies is not reflected here.

That said, however, it seems much clearer than before what the government’s fiscal situation is. Which is one reason why, possibly, the bond markets might take a very different view of the Budget from the equity markets. Market borrowing for the government in the coming year is, according to the Budget Estimates, lower than expected. The question is if the bond markets will be able to respond. Expectations that foreign investors, for example, would lap up Indian bonds have not exactly been the case in practice. As of right now, according to the Clearing Corporation of India, of the limit of Rs 2.46 trillion for the “general” category of foreign portfolio investors in Indian government securities, only Rs 1.74 trillion — just over 70 per cent — is utilised. The Reserve Bank of India has attempted to address this last month by raising the ratio of their total investment that FPIs can put into short-term securities. However, HSBC analysts have noted that “the demand dynamics for INR bonds are unlikely to change in the near term” as a consequence of the Budget, “especially with India government securities recording net selling by foreign investors in recent months”.

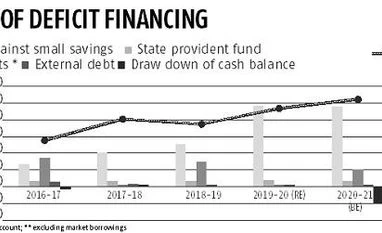

The big bonanza, however, will be if Indian bonds are included in global bond indices. In effect, this would enable funds from larger passive investors to finance Indian government deficits. The idea is that this would both ease the strain on Indian domestic resources and also avoid the dangers of dependence on short-term flows for financing government deficits. Certainly, it would be a better way of financing the deficit than depending upon the National Small Savings Fund (NSSF), which appears to be the current approach. The NSSF is being treated as a piggy bank for spending, which is clearly unsustainable.

The Budget includes some announcements that seem to be related to this effort. Ms Sitharaman’s speech included the promise that “certain specified categories of Government securities would be opened fully for non-resident investors”, though it is not yet clear what this means in practice. A related question is whether corporate bonds will also benefit; Principal Economic Advisor Sanjeev Sanyal talked about how new legislation promised for bilateral netting might help develop credit-default swaps and thus deepen the corporate bond market.

On some level, the effects on the bond and equity markets should be seen together. What is happening is that the Indian government is now stuck living beyond its means. It is not paying its bills to such entities as oil-marketing companies, fertiliser companies and the like; it is delaying payments to states; it is not following through on Budgeted discretionary and capital expenditure. As a rule of thumb, about two-thirds of the expenditure of the Union government is “tied” — it is difficult to reduce. Thus the burden of reduced revenue falls upon the remaining third of expenditure, which has been squeezed — but also upon the financial markets generally. Given that there is significant resistance to issuing dollar-denominated debt, as was made clear last year, we are left with a dependence upon domestic financial markets. The capability of the latter to finance the deficit depends upon their size, which depends in turn upon the size of financial savings of households and of foreign inflows. Higher disinvestment receipts mean that there is less financial household savings — which constitute perhaps 10 per cent of GDP — for other equity market participants to mop up. More government paper in the bond markets has traditionally had a similar crowding-out effect. Foreign participation in the equity markets is, by many people’s thinking, incentivised as much as it can be. The only path therefore left to expand the pool of finance that can prop up deficits is by increasing foreign participation in the debt market. Essentially, the government has few other options remaining. The immediate impact of the crisis is thus being felt in the government’s increased openness to foreigners financing its deficit.

There are two crucial questions left. First, if such inflows materialise, what will be the effect on the rupee’s value — and therefore on exports growth, the only sustainable path to recovery? And second, will attempts to increase this flow of funds into India effectively focus on a channel to government spending over what should be the focus — a channel from global finance to domestic private-sector, long-term investment?

m.s.sharma@gmail.com , Twitter: @mihirssharma

That said, however, it seems much clearer than before what the government’s fiscal situation is. Which is one reason why, possibly, the bond markets might take a very different view of the Budget from the equity markets. Market borrowing for the government in the coming year is, according to the Budget Estimates, lower than expected. The question is if the bond markets will be able to respond. Expectations that foreign investors, for example, would lap up Indian bonds have not exactly been the case in practice. As of right now, according to the Clearing Corporation of India, of the limit of Rs 2.46 trillion for the “general” category of foreign portfolio investors in Indian government securities, only Rs 1.74 trillion — just over 70 per cent — is utilised. The Reserve Bank of India has attempted to address this last month by raising the ratio of their total investment that FPIs can put into short-term securities. However, HSBC analysts have noted that “the demand dynamics for INR bonds are unlikely to change in the near term” as a consequence of the Budget, “especially with India government securities recording net selling by foreign investors in recent months”.

The big bonanza, however, will be if Indian bonds are included in global bond indices. In effect, this would enable funds from larger passive investors to finance Indian government deficits. The idea is that this would both ease the strain on Indian domestic resources and also avoid the dangers of dependence on short-term flows for financing government deficits. Certainly, it would be a better way of financing the deficit than depending upon the National Small Savings Fund (NSSF), which appears to be the current approach. The NSSF is being treated as a piggy bank for spending, which is clearly unsustainable.

The Budget includes some announcements that seem to be related to this effort. Ms Sitharaman’s speech included the promise that “certain specified categories of Government securities would be opened fully for non-resident investors”, though it is not yet clear what this means in practice. A related question is whether corporate bonds will also benefit; Principal Economic Advisor Sanjeev Sanyal talked about how new legislation promised for bilateral netting might help develop credit-default swaps and thus deepen the corporate bond market.

On some level, the effects on the bond and equity markets should be seen together. What is happening is that the Indian government is now stuck living beyond its means. It is not paying its bills to such entities as oil-marketing companies, fertiliser companies and the like; it is delaying payments to states; it is not following through on Budgeted discretionary and capital expenditure. As a rule of thumb, about two-thirds of the expenditure of the Union government is “tied” — it is difficult to reduce. Thus the burden of reduced revenue falls upon the remaining third of expenditure, which has been squeezed — but also upon the financial markets generally. Given that there is significant resistance to issuing dollar-denominated debt, as was made clear last year, we are left with a dependence upon domestic financial markets. The capability of the latter to finance the deficit depends upon their size, which depends in turn upon the size of financial savings of households and of foreign inflows. Higher disinvestment receipts mean that there is less financial household savings — which constitute perhaps 10 per cent of GDP — for other equity market participants to mop up. More government paper in the bond markets has traditionally had a similar crowding-out effect. Foreign participation in the equity markets is, by many people’s thinking, incentivised as much as it can be. The only path therefore left to expand the pool of finance that can prop up deficits is by increasing foreign participation in the debt market. Essentially, the government has few other options remaining. The immediate impact of the crisis is thus being felt in the government’s increased openness to foreigners financing its deficit.

There are two crucial questions left. First, if such inflows materialise, what will be the effect on the rupee’s value — and therefore on exports growth, the only sustainable path to recovery? And second, will attempts to increase this flow of funds into India effectively focus on a channel to government spending over what should be the focus — a channel from global finance to domestic private-sector, long-term investment?

m.s.sharma@gmail.com , Twitter: @mihirssharma

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in