"Dabur: Margins to come off as company pushes growth")

Dabur India (Dabur)'s consolidated March 2017 quarter (Q4) results were a bit disappointing, even as it had a few surprises for investors.

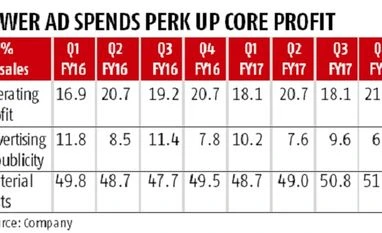

On the positive side, Dabur sustained market share gains for the second quarter in a row across its key categories such as Oral care, Hair oils, Juices and Home care, even as competitive intensity remained high. The company even managed to recover some market share lost to Patanjali in the honey segment. Secondly, as compared to analysts' expectation of a contraction, operating profit margin witnessed healthy expansion aided to some extent by falling advertisement spends (as a per cent of sales), employee costs as well as other expenses. As a result, the company's operating profit margin came in at 21.9 per cent, highest over the past 7-8 quarters.

That's where the good news ends. The 2.4 per cent domestic volume growth was a disappointment. While it comes on a high base of 7 per cent in the March 2016 quarter and was better than the decline of 5 per cent seen in Q3 indicating that much of the demonetisation-related pain is behind, the number was lower than analysts' expectations of 4-5 per cent increase. Among categories, even as hair oils grew well on the back of strong growth in Almond hair oil, Sarson Amla oil, Brahmi Amla, among others, shampoos continued to face some heat. In fact, Dabur is looking to revamp its flagship Vatika portfolio towards the Ayurveda platform. International business (one-fourth of consolidated revenues) also remained weak on the back of currency devaluation in Egyptian Pound, LIRA, etc as well as due to macro-economic headwinds faced in Saudi and UAE.

So, even as margins came better than expected and higher other income coupled with savings in interest costs helped Dabur post a net profit of Rs 333 crore (up 0.5 per cent year-on-year), it was below Bloomberg estimate of Rs 337 crore. The weaker volume number and adverse currency movement also meant that net sales at Rs 1,909 crore, down 4.8 per cent year-on-year, were also lower than expectations of Rs 2,025 crore.

Going ahead, Dabur is working to ramp up volumes, and is targeting domestic volume growth of 5-10 per cent. But, that may not be easy given the demand environment and will come at a cost. Dabur is stepping up advertisement spends, and believes operating profit margins could trend down a bit and is comfortable trading some margins for higher growth. A key monitorable though would be implementation of goods and services tax (GST) in July. While the company is well prepared to comply with and implement GST, management indicated that the various distribution channels such as wholesalers, retailers seem to be under-prepared for GST. This means the company could witness some pressure on domestic volume growth, particularly in the first half of this fiscal.

At current levels, the Dabur stock trades at 35 times one-year forward estimated earnings which is higher than its historic average of 32.1 times and seems to bake in the positives adequately.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

₹249

Renews automatically

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in