"Ebb and flow of Indian tax reform")

Indian tax administration has made successful efforts at improvement on the efficiency of customs and border management clearance, moving up from rank 65 in 2014 to 38 in 2016. On the parameter of Trading Across Borders, reforms such as the introduction of a single window interface for trade (SWIFT), electronic messaging system, filing of import and export declaration online with digital signature are said to have resulted in improvement in the indicator.

The direct tax administration has witnessed 88 per cent of the tax amount being paid through e-payment and 97 per cent of the returns being filed electronically. This too is commendable. The tax departments indicate they have examined and analysed the recommendations of the Tax Administration Reform Commission (TARC). What they have implemented or accepted are being uploaded in the Department of Revenue website. Some TARC Members also keep discussing the progress being, or not being, made.

Nevertheless, while it is not impossible to take issue with the World Bank’s index of Ease of Paying Taxes (EPT), it is salient to examine them and ponder where critical lacunae could lie in India’s tax administration practices. The exact EPT ranking may not be all important, but there are some indicators that point towards possible areas of, and need for, serious, concerted reform.

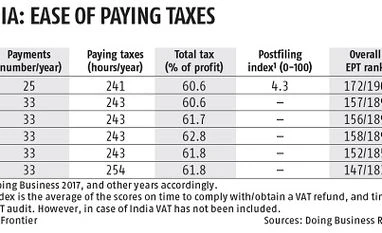

Table 1 demonstrates World Bank’s time series for India’s EPT, the most recent available year being FY15-16.The last column indicates that India’s overall rank worsened to 172 from better rankings in previous years. Interestingly, this is despite individual components of the index—number of tax payments per year, time taken for paying taxes, total tax to be paid as per cent of profit — all improved over recent years. On examination, the overall sharp worsening is due to the inclusion of a new component — post-filing index — in which India scored 4.3 out of 100.

The third last column of Table 2 reveals India’s inadequate performance in the post-filing index among BRICS, the UK and the US. This index is the average of the scores on time spent to comply with and complete a CIT audit and the time needed to comply with and obtain a VAT/GST refund. In India’s case the VAT component has not been included though one may expect it will be included once GST comes on board. Thus it is what happens “after” the filing of corporate income tax returns that is driving the worsening in the EPT score. Clearly this functional area has to remain in focus and immediate reform is crucial.

Table 2 thus reveals that India’s overall EPT ranking is worse than all except Brazil. And the hours needed on a CIT audit in India is 54 hours, higher even than Brazil’s 38.5 hours, the other countries being significantly lower. It is one thing to make tax payment mechanisms electronic, and quite another to speed up post-filing processes — where one-to-one contact between the taxpayer and the tax official is unavoidable — and make them comparable to other tax administrations. TARC strongly emphasised fixing accountability on the tax administration in completing scrutiny and audit; beyond a fixed period, it should conclude in the taxpayer’s favour. This has not occurred and time cannot be lost in quickly correcting what is occurring in the field.

The GST is being put forward as a landmark indirect tax reform aiming to simplify, harmonise and digitise the entire value chain. Given the multiple rate structure, differentiation between goods and services, and exemption of crucial inputs by excluding them from input tax credit, this will be a challenging task. To compensate for the complex structure, the tax administration appears to be assuming excessive powers to implement the GST. Soon after the GST is introduced, the World Bank’s post-filing index could be expected to include a GST refund component. One has to wait and view how India emerges in a cross-country comparison.

My continuing concerns reflect an association with Indian tax policy and administration over three decades. I view the tax administration as making selective positive efforts though TARC Members — both from within the department as well as from outside — also perceive that important elements of TARC recommendations for undertaking fundamental structural reform have been resisted or set aside. Further, new powers are being acquired that go beyond the essence of international practice such as new search and seizure rules in direct tax or rules to obviate unjust enrichment under indirect tax or GST.

As a concluding observation, both Tables 1 and 2 reveal that the Distance to Frontier — how far a country is from reaching its own potential —index (DTF) is also very low for India, better only than Brazil. Clearly, intensified effort for excellence in the field will assist in taking India closer to its own potential. My goodwill for the Indian tax administration and a conviction that an efficacious administration is achievable remain unshakeable; by the same token, I cannot desist from closely following the ebb and flow of its policies and actions.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in