To put this achievement in perspective, it may be useful to notice that according to UNCTAD (World Investment Report) data, India is now the 10th largest recipient of FDI flows, with the US being the leader having attracted $252 billion in 2018. India’s share in global cross-border investment flows has increased from 2.0 per cent in 2010 to 3.2 per cent in 2018.

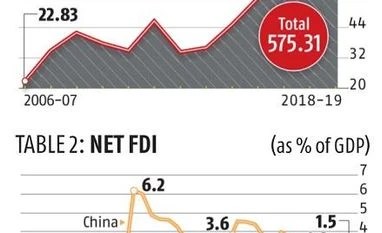

It is, however, also worth noting, that according to the World Bank data (World Development Indicators), the share of net FDI inflows in India’s GDP has less than halved over the years. It had peaked in 1999 at 3.6 per cent of GDP and has since declined to come in at 1.6 per cent in 2017 (Figure 1). Having staged a comeback in 2018-19, the share would be slightly higher today. In terms of share in GDP, India’s performance looks comparable in 2017 to both China and the US. However, this disguises the reality that with its GDP now nearly five times the size of India’s economy, China managed to attract, $129 billion in 2018 (latest available data). Moreover, it is clear that the remarkable Chinese economic performance since 1982, when it implemented its bold structural reforms, was driven by a relentless pursuit of FDI. Consequently, the share of net FDI inflows in Chinese GDP rose from about a measly 0.2 per cent in 1982 to a whopping 6.2 per cent in 1993. During this time per capita incomes in China rose from $203 to $377 and have maintained this rising trajectory ever since.

In our case, being negligible in 1982, net FDI inflows as a percentage of GDP also increased but peaked in 2008. At its peak, FDI’s share in India’s GDP was just more than half of Chinese peak levels. They were at about the same level in 1982. It is evident that we decided to reduce our dependence on foreign investors for creating additional jobs and spurring economic growth at a much earlier stage compared to our northern neighbour. In this context, it is perhaps worth pointing out here, that in 1991, per capita incomes in China and India were at somewhat similar levels (6-7 per cent) of global average per capita incomes. By 2018, Chinese per capita incomes were more than 85 per cent of global averages, while India’s per capita incomes reached up to 18 per cent of the global averages over this period. Surely, there are some lessons to be learnt from this evidence.

"FDI: Bringing all stakeholders on board")