"Hindalco prospects brighten on Novelis' strong show")

Sustained improvement in profitability and rising free cash flows for Novelis, Hindalco’s US subsidiary, are a big positive. The trend continued in the March 2017 quarter (Q4) lifting investor sentiment. The Hindalco stock gained more than four per cent intra-day before closing at Rs 193.40.

Novelis reported one of its best Ebitda (earnings before interest, tax, depreciation and amortisation) figures at $292 million, which was ahead of most analysts’ estimates. Ebitda was five per cent higher than Q4 in FY16 and 15 per cent higher sequentially, led by a better product mix and cost savings. A better profitability indicator, Ebitda per tonne of $370, was five per cent higher year-on-year (y-o-y) and nine per cent sequentially. The rising share of automotive shipments in the product mix amid benign London Metal Exchange (LME) aluminium prices continue to help Novelis.

Automotive shipments increased 26 per cent y-o-y even as total shipments of rolled aluminium products were flat y-o-y at 789,000 tonnes. Aluminium on the LME averaged at about $1,848 a tonne, up eight per cent sequentially and 22 per cent y-o-y in Q4. Higher prices also helped net sales increase nine per cent y-o-y to $2.6 billion.

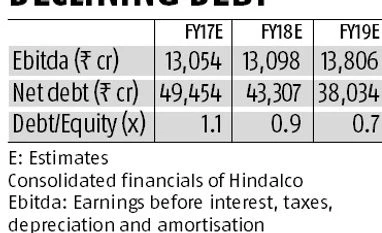

Strong profitability coupled with the refinancing of debt at lower interest rates bodes well for free cash flows (FCF; the amount of cash generated from operations available after setting aside funds for capital expenditure). Novelis, after successful bond refinancing during the second quarter, had refinanced a $1.8-billion term loan with Asian banks in January. This, it had said, will result in an extended debt maturity profile and annual cash interest savings of about $80 million. For FY17, FCF has already doubled to $316 million from $161 million in FY16. Notably, Novelis has been able to achieve a net debt to Ebitda target of 4x, one year ahead of schedule.

Wednesday’s announcement by Novelis of the sale of 50 per cent stake in its South Korean facility for $315 million and entering a joint venture with Kobe Steel, will help reduce debt further. Since the plant had remained underutilised, it will have limited impact on earnings but benefits on debt reduction will be higher, feel analysts.

Moving forward, while Novelis’ guidance remains strong, analysts are positive on sustained improvement in financials. Analysts at Edelweiss say they are upbeat on the sustained level of high spreads and Ebitda margin, and perceive further upside with auto lines ramping up. Free cash flow sustenance at high levels and improvement in debt profile are additional sweeteners.

All this only brightens Hindalco’s prospects, which is already seeing improvement in its domestic business. The debt reduction at the consolidated level could also lead to a re-rating. Analysts are already increasing their target prices and ratings. ICICI Securities and Kotak have upgraded Hindalco from Reduce/Sell to Add/Hold, while Edelweiss increased its target price to Rs 236.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in