"India's distinctive demographic dividend")

Andrew McAfee, the techno-optimist, tweeted a few days ago that the world has reached “peak children”. There will never be more of them than there are now. Encouragingly, this is not true for India, which is poised to reap the so-called demographic dividend. Using new projections of population and age structure, provided by Prof Irudaya Rajan and Dr Sunitha for this year’s Economic Survey, we present some new findings.

India’s demographic profile is distinctive: It is unique in three ways, with key implications for the growth outlook of India and the Indian states. Figure 1 compares UN projections of the ratio of the working age (WA) to non-working age (NWA) population between 1970 and 2050 for India, Brazil, South Korea, and China. This is an intuitive number because a magnitude of 1 essentially means that there are as many potential workers as dependents.

India’s demographic sweet spot is rapidly closing: The demographic dividend refers to the increase in a country’s growth potential due to having a young population. Countries with a large share of WA population appear to benefit from greater economic dynamism. Younger populations are more productive; tend to save more, which may also lead to favourable competitiveness effects; and have a larger fiscal base because of higher economic growth and fewer dependents. However, the real demographic sweet spot arises from not only a large WA/NWA ratio but also a growing one.

Extending the work of Ashoka Mody and Shekhar Aiyar, we estimate demographic dividend for India (the additional growth in per capita income due to demographic factors alone) for the next few decades. It is striking that the dividend is projected to peak in the next four years. This does not mean that the demographic dividend will turn negative; rather, the positive impact will slow down.

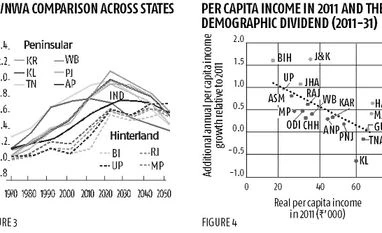

India’s demographic profile is highly heterogeneous: These aggregate projections mask considerable variation in the states’ demographic profiles and the timing and magnitude of their demographic dividend. Figure 3 shows that there is a clear divide between peninsular India (West Bengal, Kerala, Karnataka, Tamil Nadu and Andhra Pradesh) and the hinterland states (Madhya Pradesh, Rajasthan, Uttar Pradesh, and Bihar). In contrast, there was much greater uniformity in demographic profiles across the provinces in China.

Demographically speaking, therefore, there are two Indias, with different policy concerns: a soon-to-begin-ageing peninsular India where the elderly and their needs will require greater attention; and a young India where providing education, skills, and employment opportunities must be the focus. But the heterogeneity also offers possibilities of mutual help through migration as documented in this year’s Economic Survey.

Heterogeneity is on balance an equalising force with some exceptions: We compare the growth boost due to demographics for different states with their current level of per capita incomes. Figure 4 plots the two variables. The negative relationship signifies that, on average, the poorer states today have a higher growth dividend ahead of them. Therefore, the heterogeneity in the states’ demographic profiles offers an advantage. The demographic dividend could help income levels across states converge, and hence act as an equalising force.

The encouraging overall pattern hides some interesting outliers. Bihar, Jammu and Kashmir, Haryana, and Maharashtra are positive outliers (they are far above the line of best fit) in that they can expect a greater demographic dividend over the coming years. This extra dividend will help Bihar catch up to more developed states, while already rich Haryana and Maharashtra will pull further away from the average level of income per capita in India. On the other hand, Kerala, Madhya Pradesh, Chhattisgarh and West Bengal are negative outliers: their future dividend is relatively low for their current level of income. This will make the poorer states fall back unless offset by robust reforms, while the relatively rich Kerala will probably converge to the average as its growth momentum declines rapidly.

In sum, demography affords India a unique opportunity, though it is, by no means, destiny. But this window is not available indefinitely. The time to strike, to reform, to transform is now.

Arvind Subramanian is chief economic advisor. Ananya Kotia worked on this year’s Economic Survey

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in