"Lens on central bank policy statements")

Central bank policy statements are likely to dominate the conversation in trading forums this fortnight. In India of course, the Gujarat elections will also come up as a topic for discussion. The Q2 GDP numbers and attendant macro data are still being digested.

The Reserve Bank of India’s (RBI) Monetary Policy Committee (MPC) was the first among a bunch of central banks to release its statement. India’s central bank holds status quo and maintains its growth outlook but it appears to be somewhat concerned about potential inflation, going forward.

The Q2 data indicate that GDP grew at about 6.3 per cent which Fitch Ratings categorised as “weaker than expected”. However, the general consensus is that 2017-18 will see growth in the range of 6.7 per cent — this implies a rebound through the second half. The Q3 and Q4 numbers would also be boosted by a low base effect.

For what it’s worth, the trend of lower growth was broken after five successive quarters — 6.3 per cent is an improvement over the 5.7 per cent registered in Q1. Manufacturing (up 7 per cent year-on-year) and mining (up 5.5 per cent) drove the GDP. The goods and services tax (GST) led to destocking in April-June and the better July-September performance industrial may, to some extent, have been driven by restocking. Agriculture was very weak (up 1.7 per cent). Services, which contribute over 50 per cent of India’s GDP, seem weak, with contraction in November going by the Purchasing Managers Index.

There are reasons to believe larger than normal error factors exist and this preliminary estimate could change a lot. The net tax collections from the new GST are unknown and could swing either way. Since service tax has been subsumed into the GST, that adds to the likely error factor. The Ministry of Statistics and Programme Implementation has used sales tax on items outside GST to estimate likely collections by proxy.

One crude estimate is that net GST collection needs to hit Rs 100,000 crore per month to be revenue-neutral and thus, compensate for earlier service tax-plus sales tax collections. The revenue deficit of Rs 401,085 crore between April and October is almost 25 per cent above the full-year target. India’s trade deficit is now at a 35-month high at $14 billion-plus, or about 2.4 per cent of GDP. The current account deficit is expected to swell and it’s quite likely that the fiscal deficit will overshoot the Budget target.

Another error factor arises from seasonality. September saw the kick-off for the festival season this year with Durga Puja (Navratri) and it continued into October. This fell in October-November 2016. So, there may have been a bump in September 2017 consumption showing up in higher auto sales, etc.

The MPC sees positive signals in high primary market activity with Rs 49,000 crore raised in 110 IPOs between April and October. The improved ease of doing a business ranking, the new Insolvency and Bankruptcy Code (IBC) and the recapitalisation of public sector banks are the other positives.

One of the danger signals embedded in the Q2 GDP data was a fall in private final consumption expenditure growth to an eight-quarter low of 6.5 per cent. That can be balanced off by a small rise in gross fixed capital formation to 4.7 per cent.

Inflation is expected to run between 4.3 and 4.7 per cent in the second half. Food inflation may ease if there’s a good rabi crop. But crude is expected to rule at current levels, about 15 per cent higher than in April. Metal prices have risen considerably in the past four months as well. Manufacturers will try to pass on those higher input costs.

The Federal Reserve is expected to hike rates and also set in place a plan for unwinding its bloated balance sheet. The advent of a new chairperson will also lead to some nervousness. The Bank of England is struggling to curb inflation and stimulate growth in the face of Brexit uncertainty. The European Central Bank has already cut the quantum of its ongoing quantitative easing (QE) while committing to keeping the bond-buying going till September 2018. It may just hike rates. The Bank of Japan may consider a changed stance given its massive ongoing QE and a growth rebound — like the ECB, the BoJ has a negative policy rate.

Apart from this, Russia, which is one of the world’s largest commodity exporters, is expected to cut rates with inflation at a record low. Indonesia is another major emerging market and commodity producer with a key policy meeting. But Turkey has high inflation and so does Mexico.

The Gujarat elections is expected to be some sort of a bellwether for 2019. It’s been bitterly fought with the Bharatiya Janata Party throwing everything it has into the campaign. As things stand, even a narrow verdict in its favour will be considered a boost for sentiment. This Assembly election also indicates that policy next year will, very likely, be dominated by electoral considerations. One signal — the subsidy on LPG was not reduced this month, after an unbroken run of monthly reductions for the last year. More farm loan waivers, more MNREGA spending, etc. may be on the cards — the RBI flagged these as risks for fiscal slippages.

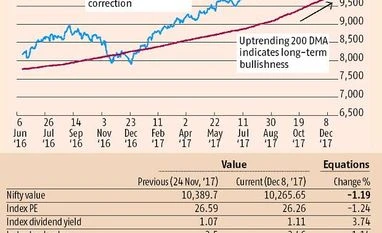

Technically speaking, the market saw a sharp correction that set up a pattern of lower lows. This could indicate further weakness especially since foreign portfolio investors are likely to be net seller through December. But the long-term trend continues to look strong with a rising 200 day moving average.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in