"Macroeconomics: Then and now")

A little over 40 years ago, when I joined the Planning Commission, Professor Sukhamoy Chakravarthi asked me to conceptualise a model for short-term macro-policy analysis. My response was in the genre of a monsoon compensation model with two sectors — agriculture and non-agricultural.

Agriculture, in the short run, was modelled as fixed quantity and flexible price sector, the fixed quantity depending on the monsoon and agricultural prices being determined by domestic demand and supply. Non-agriculture in the short run, on the other hand, was modelled as fixed price and flexible quantity sector, output and capacity utilisation being determined by effective demand given the impact of the monsoon determined agricultural growth.

A small departure from the fixed price formulation of the non-agricultural sector came through the modelling of the impact of agricultural prices on budgetary resources and on non-agricultural prices via wages and raw material costs. The impact of international terms of trade was also considered as part of cost push inflation. But given the lower ratio of international trade to GDP, this was not of great consequence, except when abnormal price shocks occurred.

This monsoon compensation model was never estimated but the conceptual structure does give an indication of the drivers of macroeconomic policy then. The challenge of short-term macro-economic management is now radically different and must take into account the following key difference between then and now:

- In the mid-seventies agriculture constituted 38 per cent of our GDP. Now that proportion is down to around 17 per cent of GDP. Monsoon compensation or income shifts arising from changes in the agriculture-non-agriculture terms of trade are not as important a consideration for macroeconomic policy.

- Exports and imports were 41 per cent of GDP in 2016-17 as against 12 per cent of GDP 40 years earlier. With a much larger part of the economy connected to the world economy and far fewer quantity controls on foreign trade, exchange rate management and fiscal and monetary policies that affect relative domestic costs become an important part of macro policy.

- From the international side, another major change is importance of private international capital flows. In the national accounts the net inflow of capital from the rest of the world as a proportion of gross fixed investment averaged to 6.8 per cent during the first five years of this decade. The gyrations of the share market are heavily influenced by foreign portfolio flows. Hence, the impact of macroeconomic policies on foreign perceptions acquires additional salience.

- In 1976-77 public sector investment was 9.8 per cent of GDP while private corporate investment was just 1.5 per cent of GDP. Managing investment 40 years ago was an internal public sector exercise. This direct ability to manage aggregate investment has been diluted by the shift in these proportions to 7.4 per cent of GDP for the public sector and 11 per cent for the private corporate sector.

Clearly, we need a different approach to macroeconomic stability in an economy that is more open, more private sector oriented and much less monsoon dependent. On the analogy of monsoon compensation we can conceptualise macroeconomic policy in an open economy as world economy compensation. This requires a clear understanding of the links between exchange rates, foreign capital flows and domestic aggregate demand supply balance.

A useful framework thinking about this is provided by a diagram first formulated by the Australian economist, Trevor Swan.

Trevor W Swan’s “Longer Run Problems of the Balance of Payments”, 1963, in H Arndt and W Corden’s The Australian Economy.

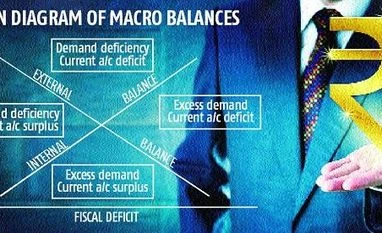

This diagram (with the original terminology modified slightly) has relative domestic prices on the vertical axis and the fiscal deficit on the horizontal axis. If domestic costs are high relative to foreign costs, there will be a current account deficit and, to ensure that domestic demand equals full employment supply, the fiscal deficit would have to be higher. That is why the internal balance line slopes upwards. The requirement for external balance is the opposite — high relative domestic costs require a tight fiscal policy to contain demand so as to keep the current account deficit in check.

Above the internal balance line there is a deficiency of demand and below it, a threat of inflation. As for external balance, above the line relative costs and/or the fiscal deficit are at a level that would lead to a current account deficit, and vice-versa below the line. Swan’s diagram was developed for a small economy with free capital flows. Hence interest rates were assumed to be set exogenously by global conditions and the need to prevent reserve depletion.

There are some modifications one has to make to apply this framework in a global economy where private capital flows have increased manifold relative to those 40 years ago. Interest rates have become an important macroeconomic policy variable and one would want to add a third axis to the domestic interest rate. External balance would now be not just on current account but also on capital account with interest rates affecting not just domestic demand but also foreign capital flows. As for internal balance, the impact of interest rates would be not just on current demand but also on growth potential.

Applying it to Indian conditions today one could argue that we are in the top quadrant — demand deficiency and a current account deficit. Moving towards a balance requires an exchange rate policy that improves relative domestic cost advantage that boosts exports and, if that is not enough of a stimulus, then some more demand boosters would be needed from fiscal measures and an interest rate reduction (controlled enough to calm nervous foreign bankers).

The broader policy message is clear. The pursuit of macroeconomic stability cannot be based on simplistic fiscal deficit or inflation targets. Exchange rate management, the interest rate set by the central bank, the fiscal stance of the government must be set in the light of prevailing global and domestic conditions rather than be bound down by unconditional rules.

Post script: Trevor Swan and I overlapped for a year at Southampton University in 1968. He had one of the sharpest minds I have ever known. As a “remembrance of times past” I offer Swan’s Way of explicating internal and external balance as a useful tool for thinking about macroeconomic policy today.

nitin-desai@hotmail.com

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in