"Making GST compliance simple: What govt plans to do and how it impacts biz")

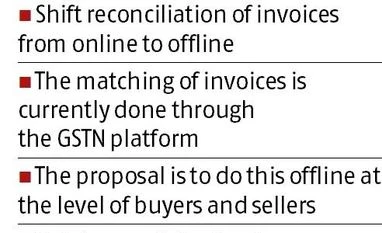

The proposed move to shift matching of invoices from the Goods and Services Tax Network (GSTN) platform to the level of buyers and sellers could turn out to be a sugar-coated bitter pill for businesses. Businesses, big and small, will have to bear the onus of higher compliance of matching invoices offline before uploading these online. In the current system, the GST Network takes over that workload.

Tax experts point out the move to shift invoice matching offline is akin to taking a step back for the GST Network. “The GST Council members are hoping that the reduction in complexity of the system will give the necessary thrust to the network to move forward and attain that critical velocity,” said a tax expert.

For many businesses offline matching of invoices is something they are familiar with. This was something they had dealt with under the VAT system in several states, experts said. To what extent the process of filing through the GST Network becomes simplified will depend on the level of details required to be filled, the periodicity of filing such returns and the mechanism to be adopted by the buyer for matching supplier invoices, among others.

“In case the onus to match the supplier invoices is cast upon the buyer, the complexity will continue or perhaps will further increase,” noted Harpreet Singh, partner, indirect tax, KPMG.

MS Mani, partner, Deloitte India, points out that there will be a far greater onus on taxpayers to ensure that their vendors are compliant if the reverse charge on composition dealers or unregistered dealers is brought into force. “The changes that will be required from a software standpoint will include a re-assessment once details of the revised compliance framework are decided in the next (council) meeting,” he added.

Both businesses and the GST Network will have to go through another round of reconfiguration of their respective IT systems in line with the process changes. “From an IT standpoint, change in the return format and mechanism will mean another round of upgrades, configuration and re-configuration,” said Singh.

A direct fallout of offline matching of invoices could mean closer scrutiny of the vendor ecosystem and preference for larger and more compliant vendors. “Businesses have to be more diligent in following up with vendors to ensure compliances and also rectify error, if any, on a timely basis,” said Pratik P Jain, partner and leader, indirect tax, PwC. This would require them to exercise greater due diligence and strengthen their compliance systems, he added.

With the power to reconcile invoices comes the responsibility to offer for audit and assessment detailed documentation of transactions. “As the onus of disclosure is on the taxpayer, audits and assessments in the initial couple of years are expected to be rigorous,” said Shrikant Kamat, leader, customs and international trade, and indirect tax partner, BDO India.

Details of stock-in-hand, work-in-progress, sales and purchase returns, credit notes, debit notes and invoices should be readily available for the purpose of audit and inspections, said experts. Thus, businesses need to ensure that their ERP systems are capable of generating transaction-level purchase and sales details in the appropriate format.

E-Way bills will come into effect from February 1. Tax experts point out that will put an additional burden on every supplier and recipient of goods with a consignment value in excess of Rs 50,000 to maintain a reconciliation of the e-way bills generated with the outward/inward supplies undertaken.

“Generating e-way bills, maintaining record and reconciliation of e-way bills could entail additional costs and upgrades to the applications,” noted Kamat.

Experts added that businesses should plan their procurement and sales schedule in advance. Last-minute modifications or cancellations could cause disruptions in the supply chain, especially for high-value consignments that required e-way bills, Kamat added.

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in