"<b>Pranjul Bhandari:</b> The Centre makes amends for states' slippages")

While much is said and written about the central government, it is the states that are responsible for over half of government spending. Eighteen major states, accounting for over 80 per cent of India's economy, have issued their Budget projections for the next fiscal year. That's enough to get a sense of what their plans might mean for overall borrowing, spending and economic growth.

We have found that steps to promote state fiscal autonomy by last year's Finance Commission (FC), which recommended how tax revenue should be shared, inadvertently led to higher than expected transfers from the Centre to the states. This can be attributed to the disruption caused by the higher proportion of "untied" (unconditional) funds that the FC championed. Several state ministries accustomed to "tied" funding suddenly realised that money was no longer coming in automatically. Halfway through the year they successfully lobbied for additional funds, resulting in higher overall transfers to states.

Yet, our study of Budget documents shows that India's states, on aggregate, exceeded their fiscal deficit targets, primarily because their in-house revenue collections disappointed, mainly due to lower taxes from falling oil prices and lower-than-expected state gross domestic product growth. The silver lining, though, was that in the face of the resource crunch, states on aggregate let their deficits slip by only 0.1 per cent of gross domestic product (GDP). They combated the remaining revenue shortfall by slashing expenditure (0.5 per cent of GDP). Encouragingly, capital spending fell only a little, since current expenditure had taken much of the hit.

Signs of prudence are also visible in the FY17 Budget estimates. The states have made much more realistic revenue assumptions this time. Alas, they seem to have under-budgeted expenditure. Recall that state governments are grappling with two new spending pressures this year: the interest payout on Ujjwal Discom Assurance Yojana (UDAY) bonds that are intended to replace power distribution companies' debt, which several states will be issuing over the next year; and the implications of the Seventh Pay Commission's (SPC) public sector wage hikes.

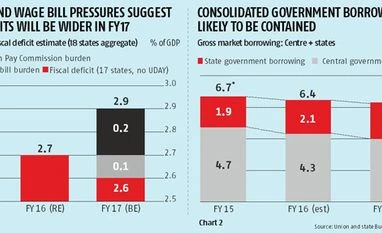

Our analysis of the central government's Budget shows that the SPC is expected to run up a bill of 0.4 per cent of GDP in FY17. Experience shows that the states' pay commission wage bill roughly equals the Centre's, even if it is spread across two years. Parsing Budget documents, we found that only a third of the states allowed for these wage hikes, among them Uttarakhand, Andhra Pradesh and Haryana. Of the remaining states, we assume that a majority will incur these as under-budgeted costs through the year and the rest will defer them. Putting these all together, the state governments' fiscal deficit is likely to be higher than last year's (chart 1).

Higher state deficits imply higher market borrowing. Before we become overly concerned, let us observe the picture in its entirety. For this, it is important to look at state borrowing alongside that of central government, especially because the Centre has been fiscally disciplined, signing up for a much smaller deficit (3.5 per cent of GDP in FY17 versus 3.9 per cent last year). The message is more comforting. As a percentage of GDP, gross borrowing is likely to remain within reasonable limits, as the discipline exhibited by the central government offsets higher state borrowings (chart 2).

To ascertain the impact on economic growth, we need a better estimate of the consolidated general government balance. According to the government's accounting methodology, the overall deficit will narrow to 6.2 per cent of GDP in FY17 (from 6.4 per cent). But this may not be accurate. We make two changes here. First, we account for asset sales and bank recapitalisation expenses as below-the-line items (technically, a preferred international practice and also a better indicator of the growth impact). Second, we make more realistic the revenue mix in the Centre's fiscal deficit estimate (we assume higher revenues from taxes, lower revenues from asset sales). With this we find that the fiscal deficit will remain unchanged at 6.9 per cent of GDP in FY17, as a higher state deficit is perfectly countered by the Centre's fiscal consolidation drive.

What does all of this mean for economic growth? Our fiscal impulse model suggests a marginally positive stimulus effect, as the deficit remains unchanged and the output gap narrows slightly over FY17. We also estimate that the state plus central government capital expenditure push is budgeted to remain unchanged, implying no worse - though no better either - quality of spending.

While the states' wider deficits - and the resulting mildly positive growth impulse - could keep economic growth from slipping, the Centre's disciplined stance could in turn keep market borrowing from soaring. Not a bad outcome.

The author is chief India economist, HSBC