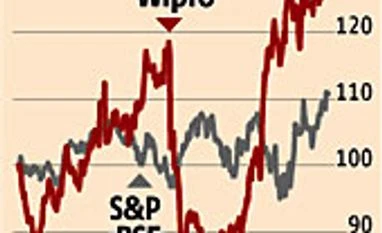

"Q2 numbers suggest Wipro is on the road to recovery")

Wipro is the latest technology company to surprise the Street, with better-than-expected numbers. The firm's dollar revenues, which imply how it has actually fared operationally during the second quarter, have grown 2.7 per cent. The dollar revenue growth has surprised the market because it is at least 50 basis points ahead of the market's estimates. This is Wipro's best revenue growth in more than seven quarters. The company says its strategy of focusing on its top clients and the front-end is yielding results.

The firm has signed 45 new clients during the quarter and one large multi-year deal with a leading banking and financial services company in the US. Wipro has also won a large multi-year contract with a leading bank in the US and the integrated IT and BPO deal further enhances Wipro's capabilities in the payments technology and payments processing domain, the company says.

Wipro expects the uptick in the banking and financial services space to continue, as discretionary spends are on the rise. The firm's optimism is reflected in its guidance for the third quarter as well. The company has guided for a revenue growth for its IT services to be between $1,660 million and $1,690 million. This guidance implies a sequential revenue growth of 1.8-3.6 per cent, which is achievable.

The market is viewing this quarter's performance as a clear turnaround, as the traction in growth is visible across verticals and geographies. For instance, while Wipro's core market has shown growth, Asia-Pacific and emerging markets have grown at 6.3 per cent sequentially (in dollar terms), which implies the company's go-to-market strategy is working.

The firm has signed 45 new clients during the quarter and one large multi-year deal with a leading banking and financial services company in the US. Wipro has also won a large multi-year contract with a leading bank in the US and the integrated IT and BPO deal further enhances Wipro's capabilities in the payments technology and payments processing domain, the company says.

Wipro expects the uptick in the banking and financial services space to continue, as discretionary spends are on the rise. The firm's optimism is reflected in its guidance for the third quarter as well. The company has guided for a revenue growth for its IT services to be between $1,660 million and $1,690 million. This guidance implies a sequential revenue growth of 1.8-3.6 per cent, which is achievable.

Also Read

It's not just the top line growth that has positively surprised the Street. Wipro's Ebit margins are up 250 basis points sequentially to 22.5 per cent. Some of this margin expansion has been driven by a 60 basis point fall in the sales and general administration expenses, explains Dhananjay Sinha of Emkay Global. Sales and other expenses have dropped 60 basis points to 12.4 of sales during the quarter. Apart from this, margins have also been impacted positively by the 11 per cent fall in the rupee during the quarter. Gross margins are up 180 basis points to 34.8 per cent quarter-on-quarter.

The market is viewing this quarter's performance as a clear turnaround, as the traction in growth is visible across verticals and geographies. For instance, while Wipro's core market has shown growth, Asia-Pacific and emerging markets have grown at 6.3 per cent sequentially (in dollar terms), which implies the company's go-to-market strategy is working.