"<b>Shankar Acharya:</b> Fiscal deficits - a short history")

Thirty years ago very few people in India had heard of “fiscal deficits”. The phrase made its debut appearance in an official government document in the 1989/90 Economic Survey of the Ministry of Finance, where it was defined as the excess of government expenditure and net lending over current revenues. It can also be thought of as “net borrowing” by the government. Within a year or two, the term had become ubiquitous in official documents, the press and political discourse, aided by the debates over International Monetary Fund programmes and economic stabilisation following the 1991 crisis. Of course, our governments had been merrily running up fiscal deficits (and the associated overhang of government debt) long before the phrase became common currency.

It might be instructive to briefly review the trajectory of fiscal deficits in India over the past 35 years, roughly the period of my association with Indian public finance. An important reason for doing so is the central importance of these deficits in macroeconomic policy and performance. Economists and other policy makers are generally agreed that large and persistent fiscal deficits are inimical to good macroeconomic performance. Such deficits tend to crowd out private investment, increase inflationary potential, weaken the balance of payments (BoP), make financial sector reform more difficult and impose a burden of debt on future generations. No wonder they say “It’s Mostly Fiscal”!

India’s fiscal deficit (Centre and states combined) has averaged 7.7 per cent of gross domestic product (GDP) for the last 35 years. In only one single year, 2007/8, did it drop below 5 per cent. That’s quite an extraordinary record of fiscal profligacy, matched by no other sizable nation on earth. In 2015, when our deficit was 7.5 per cent of GDP, Euro Area deficits averaged 2 per cent, advanced G-20 countries 3 per cent and emerging G-20 nations 4.4 per cent (and that was bloated by Saudi Arabia’s oil price slump hit a 16 per cent spike). Indeed, it is almost a miracle that despite such loose fiscal policy, India has managed average economic growth of over 6 per cent per year over the past 35 years. But before we jump to the wrong conclusion that persistent high deficits have helped our economic growth and development, let’s look at our fiscal deficit history a little more closely.

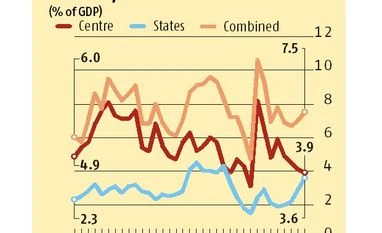

The figure shows the trajectory of deficits of the central government, states and both levels of government combined since 1981/82. Behind these three squiggly lines there are quite a few stories to be told. The combined deficit rose from an unremarkable 6 per cent of GDP in the early 1980s to 8 per cent by mid-decade and stayed in the 8-9 per cent right up to 1990/91. This heightened fiscal imbalance, entirely due to the central government, is generally believed to have been a prime cause of the 1991 balance of payments crisis. In their classic treatise, India: Macroeconomics and Political Economy, Vijay Joshi and Ian Little go even further, “…the crisis of 1990/91 and 1991/92 is wholly attributable to the lax fiscal policy of the preceding years”.

The same crisis triggered a moderately serious effort at fiscal consolidation by the central government, which brought the combined deficit down from above 9 per cent of GDP in 1990/91 to 6 per cent in 1996/97. (As before, the states’ fiscal deficit remained range-bound between 2 and 3 per cent of GDP). This reduction, together with the wide-ranging economic reforms of the early 1990s, engendered a swift revival of economic growth from just over 1 per cent in the crisis year, 1991/92, to 8 per cent in 1996/97, with the quinquennium 1992-97 registering a hitherto unprecedented 6.6 per cent average GDP growth.

India’s fiscal deficit trends are a bit like an alcoholic trying, unsuccessfully, to reform. Virtue does not last for too long. In the five years following 1996/97, the combined fiscal deficit bounced back inexorably to a peak of 9.6 per cent of GDP in 2001/2. Amongst the key culprits was the surge in government pay and pensions following the Fifth Pay Commission. Since the states followed suit with similarly generous pay and pension revisions, this time the deterioration of the combined fiscal deficit was due to widening deficits at both the central and state government levels. High fiscal deficits went with high real interest rates. Economic growth in 1997-2003 slowed to an average of 5.4 per cent, with other factors, such as the backwash of the Asian Financial Crisis (1997-1999) and a succession of weak monsoons also having negative effects on growth.

Fiscal virtue returned after 2002/3, with the next five years up to 2007/8 witnessing a major reduction in the combined fiscal deficit from 9.3 per cent of GDP in 2002/3 to a record low of 4.7 per cent in 2007/8. Favourable factors were at work at both levels of government. Parliament passed the path-breaking Fiscal Responsibility and Budget Management law in 2003 and it was notified in 2004. Following the 12th Finance Commission’s recommendations in 2004, linking debt relief to states with their enactment of similar laws, nearly all states did so. State sales taxes were converted into state value-added taxes and the Centre’s service tax base was substantially expanded. Lower fiscal deficits led to lower interest rates, which promoted higher investment and growth, which, in turn, increased revenues and thus further reduced deficits. Economic growth soared to record highs to average 8.7 per cent in 2003/8.

This remarkable fiscal consolidation was utterly negated by the pre-election fiscal populism of the Central Government in 2008/9, when massive spending hikes, including on wages and subsidies, ensured that Finance Minister P Chidambaram’s deficit target of 2.5 per cent of GDP was hugely overshot to yield an actual outcome of 8.2 per cent of GDP (including including off-Budget petroleum/fertiliser bonds), resulting in the highest combined deficit in the last 35 years, amounting to 10.6 per cent of GDP. This massive “fiscal stimulus” shored up growth for a couple of years, but at the expense of a prolonged bout of double-digit consumer inflation and growing BoP deficits.

The last seven years have seen efforts to recover from that fiscal binge, with the Centre’s efforts somewhat undercut by renewed laxity in state fiscs. The alcoholic’s struggle to reform continues… but there is long way to go.

The writer is honorary professor at ICRIER and former Chief Economic Adviser to the Government of India. Views are personal

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in