"Sun Pharma's Japan buys are small step to big gains")

Amidst negative news for the pharmaceuticals sector, Sun Pharma’s deal to acquire 14 prescription brands from Novartis AG and Novartis Pharma AG in Japan has bought some cheer. Deal valuations are attractive at 1.83 times sales, given that Sun Pharma will be paying $293 million (Rs 1,960 crore) for these brands that have annual sales of $160 million (Rs 1,070 crore). The move will significantly strengthen Sun’s limited presence in Japan, the world’s second largest health care market. So far, only Lupin has been able to crack the Japanese market — its only recently that Biocon too announced a deal that will give it inroads into Japan.

By December IMS data, the Japanese pharma market was estimated at $73 billion (seven per cent of the $1-trillion global market).

By acquiring known brands, Sun targets to build its own brand. From day one, the acquired brands will be marketed and distributed by a local marketing partner under the Sun Pharma label. At a later stage, the marketing and distribution rights could get transferred to Sun, say analysts at Credit Suisse. It is during such a stage that Sun might enter the generics space with other products.

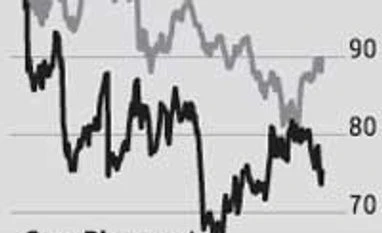

The stock was up over two per cent on Wednesday.

There are other positives, too. The company is likely to see better March quarter performance, driven by the launch of oncology drug Gleevac generics. However, the Street will be eyeing the developments on Halol plant remediation.

The company had indicated the remediation to be completed by the next quarter. This will be crucial and any cue on clearance of the plant by the US regulator will act as a trigger, leading to re-rating. Most analysts have a target price ranging from Rs 760 to Rs 900 and are likely to rework their target prices after results. The consensus target price, by analysts polled on Bloomberg since start of February, is Rs 909 for the stock trading at Rs 812.

By December IMS data, the Japanese pharma market was estimated at $73 billion (seven per cent of the $1-trillion global market).

By acquiring known brands, Sun targets to build its own brand. From day one, the acquired brands will be marketed and distributed by a local marketing partner under the Sun Pharma label. At a later stage, the marketing and distribution rights could get transferred to Sun, say analysts at Credit Suisse. It is during such a stage that Sun might enter the generics space with other products.

The stock was up over two per cent on Wednesday.

There are other positives, too. The company is likely to see better March quarter performance, driven by the launch of oncology drug Gleevac generics. However, the Street will be eyeing the developments on Halol plant remediation.

The company had indicated the remediation to be completed by the next quarter. This will be crucial and any cue on clearance of the plant by the US regulator will act as a trigger, leading to re-rating. Most analysts have a target price ranging from Rs 760 to Rs 900 and are likely to rework their target prices after results. The consensus target price, by analysts polled on Bloomberg since start of February, is Rs 909 for the stock trading at Rs 812.