"<b>Syed Zubair Naqvi, Kapil Patidar & Arvind Subramanian:</b> India's real fiscal policy for FY16")

We have since compiled new data for the states - to complement the data for the Centre - to arrive at a clearer and more accurate position of Indian public finances. And the result is to re-inforce even more strongly our three core conclusions. Consider why.

It is absolutely imperative to recognise that in the aftermath of the adoption of the recommendations of the Fourteenth Finance Commission (FFC) India's public finances must be assessed at a consolidated level by combining the finances of the Centre and the states. The reason is simple and captured in the chart "State's share in national taxes". Courtesy of the FFC, the states are expected to have and spend 62 per cent of all tax revenues collected, a jump from 55 per cent estimated for the last year (FY2015). To focus on the Centre is, therefore, to miss more than half of all the fiscal action.

There is one technicality that we must contend with. Of the 17 states for which we have data, seven of them have presented Budgets for FY2016 without taking account of the increased transfers they will receive consequent upon the FFC.2 For these states, we make plausible assumptions about how the increased transfers will be used. Specifically, we assume, partly based on the expenditure pattern of 10 states who have internalised the FFC's recommendations, that a part of the surplus resources (increased tax revenue net of reduction in plan transfers) would be used for saving and the remaining for capital expenditure in the ratio of 1/3 and 2/3, respectively

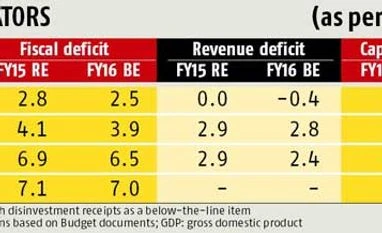

The results are presented in the table "Fiscal indicators" for our three measures of fiscal policy: the fiscal deficit (measuring aggregate consolidation); the revenue deficit (reflecting the quality of fiscal consolidation); and capital spending (reflecting the augmentation of the economy's supply potential).

Fiscal deficit: For the Centre, the deficit is budgeted to decline from 4.1 per cent of gross domestic product (GDP) in 2014-15 RE to 3.9 per cent in 2015-16 BE. For the states as a whole, the corresponding estimated change will be from 2.8 to 2.5 per cent of GDP. Combining the two, the fiscal deficit for India as a whole will decline by nearly 0.4 percentage points of GDP. Note that even if disinvestment proceeds are treated as financing (below-the-line) items, the consolidated overall deficit will decline by 0.14 percentage points of GDP.

Revenue deficit: For the Centre, the revenue deficit for FY16 is budgeted to decline marginally. However, the states will witness a sharp increase in their revenue surplus by about 0.4 percentage points of GDP. Combining the two yields an improvement in the consolidated revenue deficit of about 0.44 percentage points of GDP. It is worth emphasising that the states on average are much more prudent (lower overall deficit) and have a better quality of fiscal adjustment (revenue surplus compared with revenue deficit) than the Centre.

Capital expenditures: At a time of weak private investment, the central government's Budget was aimed at raising public investment in order to further revive the economy and catalyse private investment. Constrained, however, by the FFC recommendations, the Centre's public investment envelope was increased only by about Rs 50,000 crore or 0.2 per cent of GDP. But it turns out that the states are going to make up for the possible shortfall of the Centre. Capital expenditures by the states are budgeted to increase by nearly 0.3 percentage point of GDP, so that the economy as a whole can expect to receive an investment boost of close to Rs 1,40,000 crore or 0.5 per cent of GDP.

While updated data on public debt are not yet available, it seems likely that the debt situation of the states will exhibit an improvement even greater than that of the Centre, owing to their substantially better balance on the revenue account. So, the stock position of the Indian government will also improve.

The fear about furthering fiscal federalism (by adopting the recommendations of the FFC) was that it would undermine, or not be completely consistent with the direction of, the Centre's fiscal policy. If the Budgets recently presented by the states are any indication that fear has been allayed because on all three counts - consolidation, quality, and growth-enhancing potential - India's states have not just been consistent with the stance of the Centre, they have actually re-inforced it. On public finances, the states and the Centre appear to be partners in sync.

The authors are assistant directors and chief economic advisor respectively, in the Ministry of Finance.

Part one of the series appeared on April 10.

1. These 17 states are: Andhra Pradesh, Bihar, Chhattisgarh, Goa, Gujarat, Haryana, Jharkhand, Karnataka, Kerala, Madhya Pradesh, Odisha, Punjab, Rajasthan, Tamil Nadu, Telangana, Uttar Pradesh and West Bengal.

2. These seven states are: Gujarat, Jharkhand, Madhya Pradesh, Odisha, Punjab, Uttar Pradesh and West Bengal