"The state of the economy")

The recent (IMF) report on the Indian economy projects a gradual acceleration of growth but also draws attention to several downside risks. The report uses circumspect language about demonetisation and the botched implementation of the goods and services tax (GST) but is quite explicit on the growth impact. In medical language, the Indian economy is recovering from some recent traumas but is still convalescing and runs some risks of relapse.

The GST could have been implemented more intelligently, with the phased introduction of net-based reporting and a simpler tax structure. But the basic gains of a single tax structure in the country and a cooperative federal system for managing the GST are significant achievements with substantial long-term benefits, particularly if the rationalisation and simplification recommended by many are implemented. There was a price, which could have been less had the implementation been better prepared. But the long-term gain is substantial. However, in the case of demonetisation, one can hardly argue that the purported gains in digitisation of payments (increasingly under question) and tax compliance justify the drastic measure. Demonetisation was a badly conceived and a badly implemented measure that cost the economy dear.

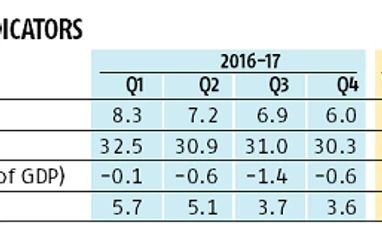

But we are a resilient government-proof people. The recovery is evident in the macroeconomic indicators as seen in the table. The growth rate of gross value added, which had dropped significantly after the demonetisation exercise, has started picking up and as has the rate of gross fixed capital formation. But the fixed investment rate is still below the 35 per cent mark achieved in 2011-12 and we are not yet seeing a revival of major project starts in the private sector. Moreover, the power sector is in serious trouble with many public and private entities on the sick list. Judging by newspaper reports, the micro, small and medium enterprises (MSME) sector also has not yet recovered from the twin traumas of demonetisation and GST implementation. As for the goal of double-digit growth, we will have to raise the investment rate to 40 per cent or more and that seems a big ask right now.

The macroeconomic indicators in the table show two key areas of concern — the revival of inflationary sentiment and a rising current account deficit. As the data shows, the consumer price inflation rate had fallen substantially till the first quarter of this year but has started rising since then. The increase in consumer prices excluding food and fuel, which are subject to supply-side disturbances — the so-called core inflation rate — has accelerated to over 6 per cent in the first quarter of this financial year. Since core inflation tends to be demand induced, the Reserve Bank of India (RBI) raised the repo rate recently. This could slow down the pace of recovery in the medium term, though the first quarter data due at the end of August may show higher growth because of a low base effect.

The rising current account deficit is a bigger source of concern. The normal inflow of foreign capital and remittances can probably finance a current account deficit of around d $50 billion, roughly the same as the deficit in 2017-18. But there are fears that this year the deficit may rise very substantially because of continued difficulties in export growth, world trade disruptions caused by the US-China trade conflicts, possible currency wars and an increase in oil prices because of the US-led sanctions on Iran. Knee-jerk reactions such as import tariff increases may compromise the productivity increases that are essential for growth acceleration.

Moving from recovery to resurgent growth will require more than just timely and far-sighted management of short-term stresses. The IMF report, as expected, argues for strengthened fiscal and monetary prudence. But for accelerating growth we should be prudent about prudence.

The IMF suggests, for instance, a reduction in the public expenditure to gross domestic product (GDP) ratio. However, as India urbanises and industrialises the need for public expenditure on infrastructure will rise more than proportionately to the GDP growth. Moreover, demands for better education, health care and social security will also require more than proportionate growth in social expenditure. Hence, prudence merits that we recognise these requirements and plan on a rising share of public expenditure in the GDP. Fiscal consolidation should aim more at raising tax buoyancy by better compliance and wider coverage, which is possible with the digitisation of the tax system and a more vigorous move in neglected areas such as property taxes and user charges.

Fiscal prudence in the form of deficit containment can play a positive role in boosting growth because it would reduce the government’s draft on private financial savings which at the moment is nearly 70 per cent. Today the government cannot afford to let go its control over about 70 per cent of banking and insurance assets as it relies on that for resources through requirements such as the statutory liquidity ratio (SLR) in banks and investment directions that serve its interests rather than those of depositors or policyholders. They are doing precisely what nationalisation was supposed to correct — the diversion of resources by owners for their own needs rather than maximising returns for depositors and policyholders. The IMF report recognises this elephant in the room but has little to add beyond the usual exhortations about better governance.

Denationalisation of public sector financial institutions is not the answer — not just for political reasons, but also because we do not have a private sector that can operate financial institutions independently of linked corporate interests. The few successful private banks that we have are independent because they are largely owned by foreign institutional investors.

Distancing public sector banks and insurance companies from direct governmental control will lead to a healthier capital market. It can reduce future non-performing asset risks, enlarge and strengthen the debt market and ensure depoliticised oversight over corporate management by major domestic institutional investors such as Life Insurance Corporation. This is essential for accelerating growth in the medium term and making other areas of structural change more acceptable and easier to implement. If we can liberate monetary policy from political control, why can we not do the same for supervision of public sector financial institutions?

nitin-desai@hotmail.com

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹8/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in