"Thumb on the scale")

The recent attempt by investors to defenestrate managements and directors and vote down a number of resolutions has markets animated about shareholder activism. And while the investor crusade has taken root and is here to stay, I expect to see the occasional flare-up, louder than before no doubt, but not an endless firework display.

This is so for a few reasons. First, just 8 per cent of the NSE-500 companies are institutionally-owned and widely held. Add at max, another 50 companies where promoter holding is at 27 per cent or below (I will come back to why this number). This implies that there are only a handful of companies that have their flanks open, and are subject to activism as it is more commonly defined. The number of companies with low or no promoter holding is set to increase, but we are not there yet. The experience with the insolvency regime and some recent episodes in the equity market are evidence of the challenges of prising away incumbent owner-managers.

Two, while the narrative about the narrowing gap between the promoter’s equity holding and that of the institutions is driven by the market cap numbers, the share ownership numbers tell a different story when aggregated across listed companies. The market cap figures for the NSE-500 tells us that over the past decade, family ownership has come down from 60 per cent to 50 per cent, while the share of institutional shareholders has increased from 22 per cent to 35 per cent. In contrast, counting each share tells us that for the last five years, promoter ownership has been at around 55 per cent, while that of the institutional shareholders at 27 per cent (explanation for why this number is used above). This ownership pattern determines voting outcomes.

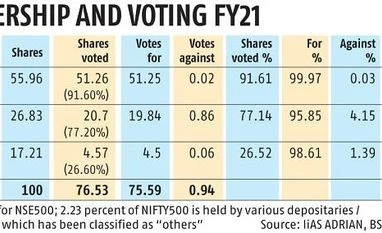

Third is the actual voting itself. In FY21, promoters as a category in aggregate voted 91.6 per cent of their shares, institutional shareholders 77.2 per cent, and others, which includes retail, voted just 26.6 per cent of their holding. Put differently, 67 per cent of the total votes cast are by promoters, and just under half this number by institutional investors (27 per cent) and others (6 per cent).

Now overlay this with how all three categories have voted. In FY21, almost the entire promoter votes are for the resolution being proposed (99.9 per cent) — unless there is family spat — institutional shareholders (95.8 per cent) and others (96.8 per cent) are habitually supportive of managements. Such voting behaviour is to be expected, since what is in the interest of the largest shareholder, must be in the interest of the minority. Its where such alignments are broken, that investors need to raise their voice. Unfortunately, as the data shows, even if all shareholders are opposed to the promoters, the promoters are still more likely to prevail.

This explains what might normally be considered an egregious resolution getting approved or why the handful of resolutions that are defeated make headlines: 194 of the 48,000+ resolutions (less than 0.5 per cent) assessed by IiAS in the last six years have been turned down.

In India, the regulators’ focus rightly is on control through the voting mechanism. They use two approaches. One, special resolutions, which need 75 per cent of the votes in favour. The other is “majority of minority”, where only the “uninterested” investors get to vote. A variation in some markets is dual voting, where you need majority of both promoters and non-promoters supporting a resolution.

Should regulators endorse a voting structure where populist vote subverts shareholder democracy? Should they ignore the vote and focus on the process? There is no right answer. But if promoters have their thumb on the voting scale, regulators have no option, but to raise the guardrails.

Regulations need to revisit which voting threshold should a resolution cross? Currently, related-party transactions need a majority of minority shareholder to approve a resolution and from the next calendar year, appointment or removal of all independent directors will be via a special resolution. What about compensation paid to promoters? Currently, these are ordinary resolutions and need a simple majority to carry. Should these continue as ordinary resolutions? Should such approvals be by way of a special resolution? Or should the promoters not be allowed to vote on their salary increase i.e., seek majority of minority vote? Many other resolutions need a relook.

Meanwhile, the activist investor will contentedly watch the number of institutionally-owned and professionally-managed companies going up, institutional voting percentages rising where the against vote is inching up. To them these numbers are an important yardstick, but more critical is that attitudes are changing. They will be feeling the tailwind behind them.

The writer is with Institutional Investor Advisory Services India Limited. Views are personal. Twitter: @AmitTandon_in

To read the full story, Subscribe Now at just Rs 249 a month

Already a subscriber? Log in

Subscribe To BS Premium

MONTHLY₹9/day

₹249

Renews automatically

SMART ANNUAL₹5/day

₹1699₹1999

Opt for auto renewal and save Rs. 300 Renews automatically

ANNUAL₹6/day

₹1999

What you get on BS Premium?

-

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app.

Unlock 30+ premium stories daily hand-picked by our editors, across devices on browser and app. -

Pick your 5 favourite companies, get a daily email with all news updates on them.

Pick your 5 favourite companies, get a daily email with all news updates on them. '%3E%3Cg id='Artboard-Copy' transform='translate(0 0.012)'%3E%3Cg id='_126115' transform='translate(0 0)'%3E%3Cpath id='Path' d='M17.537 1.487a.473.473 0 0 0-.467.477v12.67A2.4 2.4 0 0 1 14.7 17.06H3.3A2.4 2.4 0 0 1 .933 14.634V.966H14.587v12.29a.467.467 0 0 0 .933 0V.489a.473.473 0 0 0-.467-.477H.467A.473.473 0 0 0 0 .489V14.63a3.346 3.346 0 0 0 3.3 3.382H14.7A3.346 3.346 0 0 0 18 14.63V1.965a.467.467 0 0 0-.462-.478Z' transform='translate(0 -0.012)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-2' d='M12.676 3.955a.478.478 0 1 0 0-.955H2.508a.478.478 0 1 0 0 .955Z' transform='translate(0.124 0.166)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-3' d='M12.676 13H2.508a.478.478 0 1 0 0 .955H12.672a.478.478 0 1 0 0-.955Z' transform='translate(0.124 0.768)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Shape' d='M2 6v5.371a.484.484 0 0 0 .467.5H7.531a.484.484 0 0 0 .467-.5V6a.484.484 0 0 0-.467-.5H2.467A.484.484 0 0 0 2 6Zm.933.5H7.066v4.375H2.933Z' transform='translate(0.122 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-4' d='M12.321 5.5H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.317)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-5' d='M12.321 8H8.967a.478.478 0 1 0 0 .955h3.354a.478.478 0 1 0 0-.955Z' transform='translate(0.517 0.467)' fill='%23c4132a'%3E%3C/path%3E%3Cpath id='Path-6' d='M12.788 10.977a.473.473 0 0 0-.467-.477H8.967a.478.478 0 1 0 0 .955h3.354a.471.471 0 0 0 .467-.478Z' transform='translate(0.517 0.617)' fill='%23c4132a'%3E%3C/path%3E%3C/g%3E%3C/g%3E%3C/g%3E%3C/svg%3E) Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006.

Full access to our intuitive epaper - clip, save, share articles from any device; newspaper archives from 2006. Preferential invites to Business Standard events.

Preferential invites to Business Standard events. Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Curated newsletters on markets, personal finance, policy & politics, start-ups, technology, and more.

Need More Information - write to us at assist@bsmail.in