"Why analysts prefer Infosys over TCS")

The Street wasn’t expecting any fireworks from Indian information technology (IT) majors in the current times of uncertainties over global economic growth. But, unlike its larger peer Tata Consultancy Services (TCS), Infosys delivered a good set of numbers for the September quarter (Q2). It beat Street expectations on all fronts — revenues, margins as well as earnings; TCS fell short on revenue expectations but delivered better-than-expected margins and earnings. Nevertheless, Infosys’ constant currency dollar revenue growth and volumes grew 3.9-4 per cent sequentially, much better than 1-1.3 per cent reported by TCS. Infosys’ new deal wins in Q2 together are worth over $1 billion. Sadly, the dissimilarity ended here.

Toeing the line of TCS, which has become increasingly cautious on the road ahead, Infosys, too, cut its full-year constant currency revenue growth forecast from 10.5-12 per cent given in July to 8-9 per cent currently. Notably, this is the second time Infosys has toned down its forecast. Order cancellation from Royal Bank of Scotland and client-specific issues were key factors for the cut. The revised forecast implies flattish revenue growth in the next two quarters, estimate analysts.

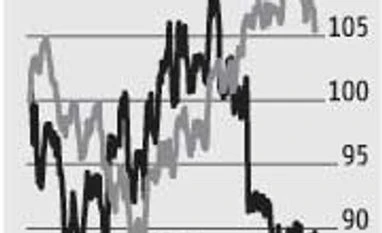

Not surprisingly, the Infosys stock fell 2.3 per cent in Friday’s trade and hit a new 52-week low of Rs 996.15 (before closing at Rs 1,027.40 on the BSE), even as TCS stock recovered some of the losses made on Thursday. At current levels, Infosys stock trades at 16 times the FY17 estimated earnings or 10 per cent lower than TCS’ valuations. This gap could reduce going forward, as Infosys’ revised forecast is higher than the 7.5-8 per cent revenue growth analysts now expect from TCS this financial year. Notably, Infosys’ management commentary is cautiously optimistic, and reflects the underlying confidence about future growth. Most analysts remain more positive on Infosys.

The Indian IT sector is going through a structural change, as it realigns its business model to the next growth engine of digital. Macro headwinds such as Brexit and US elections have only added to the woes. Though Infosys’ exposure to Europe is among the lowest, that of TCS is on the higher side. Coming quarters will be a test of Street’s faith on Infosys. The strategies and agility with which both the companies adapt to the changing macro scenario will determine their prospects. Thus, though patient investors can consider Infosys after the correction, next few quarters will be crucial, as there will be more clarity on how the macro headwinds unfold.

Toeing the line of TCS, which has become increasingly cautious on the road ahead, Infosys, too, cut its full-year constant currency revenue growth forecast from 10.5-12 per cent given in July to 8-9 per cent currently. Notably, this is the second time Infosys has toned down its forecast. Order cancellation from Royal Bank of Scotland and client-specific issues were key factors for the cut. The revised forecast implies flattish revenue growth in the next two quarters, estimate analysts.

Not surprisingly, the Infosys stock fell 2.3 per cent in Friday’s trade and hit a new 52-week low of Rs 996.15 (before closing at Rs 1,027.40 on the BSE), even as TCS stock recovered some of the losses made on Thursday. At current levels, Infosys stock trades at 16 times the FY17 estimated earnings or 10 per cent lower than TCS’ valuations. This gap could reduce going forward, as Infosys’ revised forecast is higher than the 7.5-8 per cent revenue growth analysts now expect from TCS this financial year. Notably, Infosys’ management commentary is cautiously optimistic, and reflects the underlying confidence about future growth. Most analysts remain more positive on Infosys.

The Indian IT sector is going through a structural change, as it realigns its business model to the next growth engine of digital. Macro headwinds such as Brexit and US elections have only added to the woes. Though Infosys’ exposure to Europe is among the lowest, that of TCS is on the higher side. Coming quarters will be a test of Street’s faith on Infosys. The strategies and agility with which both the companies adapt to the changing macro scenario will determine their prospects. Thus, though patient investors can consider Infosys after the correction, next few quarters will be crucial, as there will be more clarity on how the macro headwinds unfold.